ในปัจจุบันมีการแบ่ง CBDC โดยใช้เกณฑ์ด้านต่างๆ ทั้งรูปแบบธุรกรรม ระดับการมีส่วนร่วมของภาคเอกชน การจ่ายดอกเบี้ย หรือการแบ่งเกณฑ์โดยเทคโนโลยีที่ใช้ในแต่ละขั้น สำหรับการแบ่งโดยใช้รูปแบบธุรกรรมนั้น สามารถแบ่ง CBDC ได้เป็น Wholesale CBDC ที่ใช้ทำธุรกรรมระหว่างธนาคารกลางกับธนาคารพาณิชย์หรือสถาบันการเงินอื่นๆ และ Retail CBDC ซึ่งใช้ทำธุรกรรมรายย่อย ที่เกิดขึ้นระหว่างธนาคารกลางหรือภาคผู้ให้บริการทางการเงินเอกชนกับประชาชน อันที่จริงแล้วเริ่มมีการพัฒนา CBDC มาตั้งแต่ช่วงปี 2017 ซึ่งในปัจจุบันมีประเทศบาฮามาส ไนจีเรีย จาไมกา และประเทศในหมู่เกาะแคริบเบียน ที่ประกาศใช้สกุล CBDC อย่างถูกกฎหมาย เพื่อให้สามารถแก้ปัญหาระบบการทำธุรกรรมทางการเงินที่ยังไม่มีประสิทธิภาพภายในประเทศ รวมไปถึงแก้ปัญหาการเข้าถึงบริการธนาคารที่ยังติดขัดในประเทศเหล่านั้นได้อย่างมีประสิทธิภาพมากขึ้น อีกทั้งยังมีอีกหลายประเทศที่กำลังอยู่ในกระบวนการพัฒนาโดยอยู่ในขั้นตอนต่างๆ เนื่องจากเล็งเห็นศักยภาพของ CBDC ที่จะช่วยให้การทำธุรกรรมทางการเงินในโลกดิจิทัล ทั้งธุรกรรมในประเทศและธุรกรรมระหว่างประเทศมีประสิทธิภาพมากขึ้น และสามารถต่อยอดไปเป็นนวัตกรรมทางการเงินใหม่ๆ ได้อีกด้วย อย่างไรก็ตาม บางประเทศอย่างเอกวาดอร์ และเซเนกัล ที่เป็นหนึ่งในผู้บุกเบิก CBDC รุ่นแรกๆ กลับต้องม้วนเสื่อพับโครงการไปในเวลาไม่นาน

CBDC เป็นอีกหนึ่งช่องทางที่จะเข้ามาช่วยอำนวยความสะดวกให้กับการทำธุรกรรมทางการเงินในสังคมให้มีประสิทธิภาพมากขึ้น เนื่องจากคุณลักษณะเด่นของ CBDC ที่ออกโดยธนาคารกลางของแต่ละประเทศ รวมไปถึงศักยภาพของ CBDC ที่เป็นสกุลเงินดิจิทัล ยิ่งทำให้เกิดแรงกระตุ้นต่อการพัฒนา CBDC ที่นำไปสู่นวัตกรรมใหม่ๆ ผ่านการใช้เทคโนโลยีได้สะดวกขึ้น อย่างไรก็ตาม ยังมีประเด็นที่ควรพิจารณา อาทิ การพัฒนา CBDC ให้สามารถใช้งานได้ผ่านระบบออฟไลน์เพื่อตอบสนองกลุ่มผู้ใช้งานที่อาจเข้าไม่ถึงอินเทอร์เน็ตและที่ผ่านมาไม่สามารถใช้บริการ Mobile/Internet banking ได้ รวมไปถึงการพัฒนา CBDC ให้มีประสิทธิภาพเพียงพอเพื่อเตรียมพร้อมสำหรับการใช้งานได้บนโลกเสมือนจริงในอนาคต ในโลกยุคโลกาภิวัตน์ที่ทุกอย่างถูกขับเคลื่อนไปอย่างรวดเร็วและดำรงอยู่บนความไม่แน่นอน มนุษย์เราต่างหาช่องทางและโอกาสที่จะสามารถผลักดันตนเองให้ไปอยู่ในจุดที่ดีขึ้น รวมถึงในภาคการลงทุนที่ในปัจจุบันเทคโนโลยีได้เข้ามามีบทบาทและก่อให้เกิดการพัฒนาอย่างก้าวกระโดดในการช่วยสร้างรายได้ให้อีกด้วย การลงทุนในเงินคริปโต (Cryptocurrency)[1] หรือสินทรัพย์ดิจิทัลอื่นๆ จึงได้รับความนิยมอย่างแพร่หลาย จนมีหลายกระแสเก็งว่าเงินคริปโตและสินทรัพย์ดิจิทัลอื่นๆ กำลังจะก้าวเข้ามาแทนที่เงินสด (Fiat money) หรือเงินอิเล็กทรอนิกส์ (E-money)[2] ในอนาคต นอกจากนี้ ประสิทธิภาพของเทคโนโลยีการเก็บข้อมูลและประมวลผลอย่างบล็อกเชน (Blockchain) ยังอาจจะเข้ามาลดบทบาทของสถาบันการเงินในฐานะที่เป็นตัวกลาง (Intermediary) อีกด้วย สถาบันการเงินทั่วโลกต่างเล็งเห็นถึงพัฒนาการของโลกการเงินดิจิทัลที่กำลังเข้ามามีบทบาททั้งในส่วนของภาครัฐและภาคเอกชน ส่งผลให้ทั้งธนาคารกลางและธนาคารพาณิชย์ในหลายประเทศเริ่มศึกษาการนำเทคโนโลยีบล็อกเชนเข้ามาเพิ่มประสิทธิภาพทางการเงินอย่างจริงจัง โดยในฟากของธนาคารกลางนั้นมีบางประเทศที่ได้พัฒนาไปสู่การทดลองใช้สกุลเงินดิจิทัลที่ออกโดยธนาคารกลาง (Central Bank Digital Currency: CBDC) ของประเทศนั้นๆ อย่างเป็นทางการ พัฒนาการด้านการชำระเงินระลอกนี้ที่นำโดยธนาคารกลาง ทำให้หลายฝ่าย ไมว่าจะเป็นธนาคารพาณิชย์ สถาบันการเงินอื่นๆ ตลอดจนประชาชน เริ่มตั้งคำถามว่า CBDC ที่ธนาคารกลางออกมานั้นจะส่งผลอย่างไรต่อระบบการชำระเงิน การทำธุรกรรม ตลอดจนการใช้ชีวิตประจำวันของเราในอนาคตบ้าง

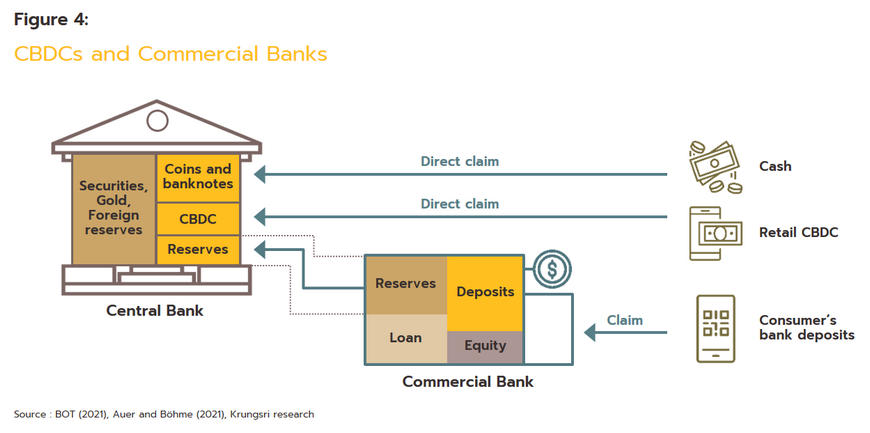

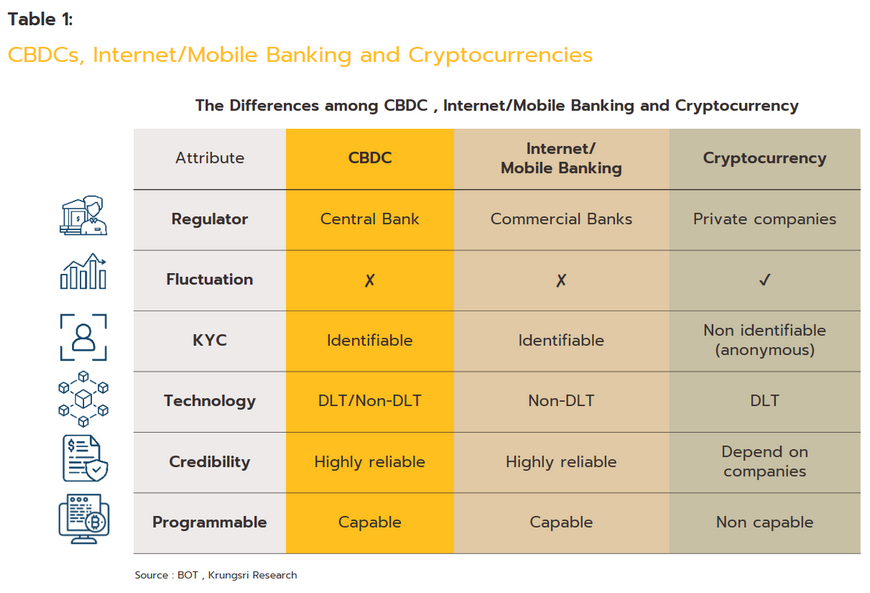

ภาพรวมและที่มาของสกุลเงินดิจิทัลที่ออกโดยธนาคารกลาง (CBDC) CBDC หรือ Central Bank Digital Currency คือสกุลเงินดิจิทัลที่ออกโดยธนาคารกลางของแต่ละประเทศ เช่นในบริบทประเทศไทย ธนาคารแห่งประเทศไทย (ธปท.) จะเป็นผู้ออก ซึ่ง CBDC นี้จะมีสถานะเป็นเงินตราที่สามารถชำระหนี้ได้ตามกฎหมายจึงสามารถนำมาใช้งานได้เช่นเดียวกับเงินสดที่อยู่ในรูปแบบเหรียญหรือธนบัตรที่ใช้กันอย่างแพร่หลายทั่วโลกมาหลายร้อยปี โดยในช่วงแรกก่อนที่จะมีการประกาศใช้สกุลเงินดิจิทัลนี้อย่างเป็นทางการ ธนาคารกลางของประเทศจะเสริมความมั่นใจให้กับประชาชนโดยการกำหนดมูลค่าของสกุลเงินดิจิทัลดังกล่าวโดยอิงกับมูลค่าเงินสกุลปัจจุบันในประเทศ เพื่อให้ประชาชนที่ถือ CBDC มั่นใจว่าเงินดิจิทัลของตนมีมูลค่าที่สามารถแลกเปลี่ยนเป็นเงินสดได้จริง ทั้งนี้ เนื่องจาก CBDC ถูกตรึงมูลค่าไว้เท่ากับสกุลเงินของประเทศนั้นๆ จึงไม่มีความผันผวนด้านมูลค่า (Value fluctuation) เหมือนสินทรัพย์ดิจิทัลอย่างเงินคริปโต ดังนั้นจึงอาจกล่าวได้ว่า CBDC มีวัตถุประสงค์หลักในการอำนวยความสะดวกให้กับผู้ใช้งาน มิใช่เป็นสินทรัพย์ดิจิทัลที่ซื้อมาเพื่อการลงทุนหรือเก็งกำไร

ในการใช้งานนั้น หากมองเพียงผิวเผิน การชำระเงินด้วย CBDC อาจจะเหมือนการใช้แอปพลิเคชันธนาคารในโทรศัพท์มือถือ (Mobile banking) หากแต่ Mobile banking นั้นเป็นบริการที่ดำเนินการโดยธนาคารพาณิชย์ ต่างจาก CBDC ที่ดำเนินการโดยธนาคารกลาง นอกจากนี้ สกุลเงินในการทำธุรกรรม 2 แบบยังแตกต่างกัน เนื่องจากการทำธุรกรรมผ่าน Mobile banking หรือแม้แต่ Internet banking ยังเป็นการทำธุรกรรมผ่านสกุลเงินเช่นเดียวกับเงินสดในมือ แต่การทำธุรกรรมด้วย CBDC จะอยู่ในสกุลเงินดิจิทัล ซึ่งถือว่าเป็นเงินสกุลใหม่ แม้จะมีมูลค่าอิงกับเงินตราของประเทศนั้นๆ ก็ตาม อีกทั้ง CBDC ยังแตกต่างจาก Stablecoin[3] และ E-money ที่มีผู้ออก (Issuer) เป็นผู้ประกอบธุรกิจในภาคเอกชนอีกด้วย

.

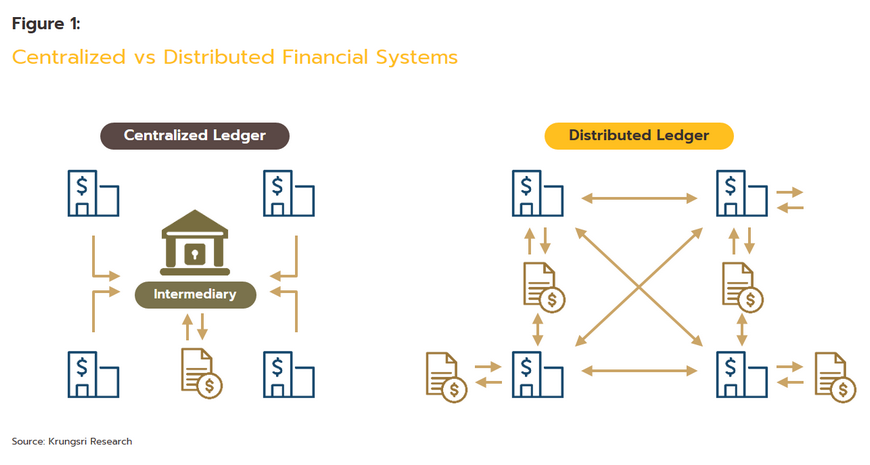

ในการพัฒนา CBDC ช่วงแรกๆ นั้น มักจะมีบริษัทผู้เชี่ยวชาญด้านการพัฒนาสินทรัพย์ในระบบดิจิทัลเข้ามาเป็นหุ้นส่วนทางเทคโนโลยี (Technology Partnership) กับธนาคารกลางเพื่อพัฒนาและทดสอบระบบ และการพัฒนาสกุลเงินดิจิทัลนี้ จะพัฒนาทั้งบนระบบธนาคารที่เก็บข้อมูลของลูกค้าไว้ที่ศูนย์กลาง (Centralization) เช่น ธนาคารพาณิชย์โดยทั่วไป และพัฒนาบนระบบ Distributed Ledger Technology (DLT) ซึ่งเป็นเทคโนโลยีแบบกระจายศูนย์(Decentralization) ที่สมาชิกสามารถแลกเปลี่ยนข้อมูลกันได้โดยไม่ต้องผ่านตัวกลางใดๆ

.

.

.

.

.

.

.

.

.

.

ช่องที่ 1: สกุลเงินดิจิทัลของ Facebook เป็นก้าวสำคัญหรือเป็นเพียงความฝันลมๆ แล้งๆ

Diem หรือชื่อเดิมว่า Libra เป็นสกุลเงินดิจิทัลที่ Facebook เปิดเผยต่อโลกในปี 2020 Libra หรือ LBR เป็นเหรียญ Stablecoin ที่ได้รับการสนับสนุนจาก Fiat ซึ่งจบลงด้วยโครงสร้างในลักษณะที่เหรียญบางเหรียญเชื่อมโยงกับ สกุลเงินเดียวในขณะที่สกุลเงินอื่นได้รับการสนับสนุนจากตะกร้าเหล่านี้ มูลค่าของราศีตุลย์จึงถูกกำหนดผ่านสองระบบ

- Stablecoins ที่สนับสนุนหลายสกุลเงิน: เริ่มแรก Libra ได้รับการสนับสนุนโดยตะกร้าสกุลเงิน แม้ว่าส่วนผสมจะถ่วงน้ำหนักไปที่สกุลเงินจากเศรษฐกิจหลักที่มีผลกระทบอย่างมีนัยสำคัญทั่วโลก เช่น ดอลลาร์สหรัฐ ยูโร ปอนด์สเตอร์ลิง เยน และเงินหยวน นี่คือโครงสร้างของ Libra เมื่อเปิดตัวครั้งแรก

- เหรียญ Stablecoin สกุลเงินเดียวที่ได้รับการสนับสนุน: ในรูปแบบที่สอง เหรียญ Libra ได้รับการสนับสนุนโดยสกุลเงินเดียวซึ่งตรึงไว้ที่อัตราแลกเปลี่ยน 1:1 แม้ว่าเหรียญจะออกเมื่อเทียบกับสกุลเงินต่างๆ ดังนั้น ในทางทฤษฎีแล้ว เหรียญ Libra ที่ได้รับการสนับสนุนจาก USD สามารถแลกเปลี่ยนได้ที่มูลค่า 1:1 เมื่อเทียบกับ USD เหรียญที่มีสกุลเงิน GBP นั้นสามารถแลกเปลี่ยนได้ที่มูลค่า 1:1 เมื่อเทียบกับ GBP และอื่น ๆ การเปลี่ยนมาใช้เหรียญสกุลเงินเดียวมีขึ้นในเดือนพฤศจิกายน 2020 หลังจากการคัดค้านโดยทางการต่อแผนเริ่มต้นสำหรับเหรียญที่รองรับหลายสกุลเงิน และความพยายามที่ตามมาเพื่อลดขนาดของโครงการ

ในขั้นต้น Facebook ต้องการเห็น Libra กลายเป็นสกุลเงินดิจิทัลที่ได้รับความไว้วางใจในระดับ CBDC แม้ว่าข้อเท็จจริงที่ว่าสกุลเงินดังกล่าวสร้างขึ้นจากชื่อเสียงที่มีร่วมกันของธนาคารกลาง สิทธิตามกฎหมายในการออกสกุลเงินของประเทศ บทบาทที่ธนาคารกลาง มีบทบาทในการควบคุมระบบการเงิน ประสบการณ์หลายทศวรรษ (ในหลายกรณีหลายศตวรรษ) ที่พวกเขามีการจัดการวิกฤตการณ์ทางการเงิน และประสบการณ์และความเชี่ยวชาญของสถาบันจำนวนมากที่พวกเขาสั่งสมมา ในขณะที่พยายามเลียนแบบสิ่งนี้ Facebook จึงสร้างสมาคม Libra ซึ่งเป็นองค์กรไม่แสวงหาผลกำไรที่รวบรวมตัวแทนจากธุรกิจ 27 แห่งที่มาจากหลากหลายอุตสาหกรรม และตั้งใจที่จะดูแลการพัฒนา Stablecoin ใหม่ในอนาคต ดังนั้น Andressen Horowitz, Thrive Capital และ Rabbit Capital จึงมาจากโลกแห่งการลงทุน ผู้เล่นบล็อกเชนมีตัวแทนจาก Coinbase และ Anchorage, eBay และ Mercado Libre มาจากอุตสาหกรรมอีคอมเมิร์ซ องค์กรที่ไม่หวังผลกำไรเป็นตัวแทนของ Women’s World Banking, Kiva และ Mercy corps และ Mastercard, PayU, PayPal, Stripe และ Visa เป็นตัวแทนของภาคการเงิน การเข้าสู่สโมสรชั้นยอดนี้มาพร้อมกับค่าธรรมเนียมแรกเข้า 10 ล้านเหรียญสหรัฐ ซึ่งแลกเปลี่ยนเป็นโทเค็นการลงทุนของ Libra และสิ่งนี้ทำให้ผู้เข้าร่วมมีสิทธิ์ในการบำรุงรักษา จัดการ และควบคุมการพัฒนาของ Libra

อย่างไรก็ตาม Facebook ประสบปัญหาอย่างรวดเร็วในรูปแบบของการต่อต้านอย่างแข็งกร้าวจากทั้งรัฐสภาสหรัฐและรัฐบาลทั่วโลก ซึ่งกลัวว่าเนื่องจาก Libra ได้รับการสนับสนุนจากเงินดอลลาร์สหรัฐและสกุลเงินอื่น ๆ การอนุญาตให้ใช้จะทำให้เกิดความเสี่ยงในการเรียกใช้ สกุลเงินภายนอกควบคู่กับสกุลเงินในประเทศ เช่น อนุญาตให้ทำเศรษฐกิจแบบดอลล่าร์ สิ่งนี้จะสร้างสถานการณ์ที่อาจเป็นอันตรายได้ เนื่องจากสกุลเงินดิจิทัล เช่น Libra ไม่ได้อยู่ภายใต้การควบคุมของรัฐบาลหรือธนาคารกลาง ดังนั้น ความสามารถของเจ้าหน้าที่ในการมีอิทธิพลต่อเศรษฐกิจในประเทศอาจถูกกัดเซาะอย่างมีนัยสำคัญ นอกจากนี้ การอนุญาตให้ใช้สกุลเงินเช่น Libra น่าจะทำให้ง่ายต่อการหลบเลี่ยงการควบคุมทางกฎหมาย ตัวอย่างเช่น การฟอกเงิน เป็นต้น นอกเหนือจากสหรัฐอเมริกาแล้ว ประเทศต่างๆ รวมถึงฝรั่งเศสและเยอรมนีคัดค้านการสร้างสกุลเงินอย่างรุนแรง . ผลที่สุดของสิ่งนี้คือ บริษัทต่างๆ เช่น PayPal, MasterCard และ eBay ซึ่งประกาศว่าจะเข้าร่วมในโครงการนี้ ได้ถอนตัวออกจากโครงการ

ในตอนท้ายของปี 2021 Facebook เปลี่ยนชื่อเป็น Meta ซึ่งเป็นส่วนหนึ่งของความพยายามของบริษัทในการเน้นย้ำถึงความมุ่งมั่นที่มีต่อ metaverse แต่ถึงแม้จะมีสิ่งนี้และการรีแบรนด์ของ Libra เป็น Diem ในช่วงสิ้นปี 2020 บริษัทก็ล้มเหลวในการเอาชนะศัตรูจากสหรัฐฯ สภาคองเกรสหรือการต่อต้านอย่างต่อเนื่องจากหน่วยงานกำกับดูแล รวมถึงเฟด[4] ยิ่งไปกว่านั้น David Marcus ผู้บริหารระดับสูงของ Meta ซึ่งมีความเชี่ยวชาญอย่างมากเกี่ยวกับ fintech และเป็นผู้รับผิดชอบการเปิดตัว Libra/Diem ครั้งแรก ประกาศว่าเขาจะออกจาก Meta ในเดือนธันวาคม 2021 สิ่งนี้ทำให้โครงการขุ่นมัวยิ่งขึ้น อนาคตที่มีปัญหาอยู่แล้ว และอาจหลีกเลี่ยงไม่ได้ Meta ประกาศว่าโครงการ Diem จะยุติลงอย่างเป็นทางการในวันที่ 31 มกราคม พ.ศ. 2565 โดยมีทรัพย์สินและทรัพย์สินทางปัญญาที่เชื่อมโยงกับระบบการชำระเงินที่ขายให้กับ Silvergate Capital[5]

ประเภทของ CBDC

CBDC สามารถจัดหมวดหมู่ตามแกนต่างๆ ได้หลายแกน และวิธีการหลักในการจำแนกเหล่านี้แสดงไว้ด้านล่าง

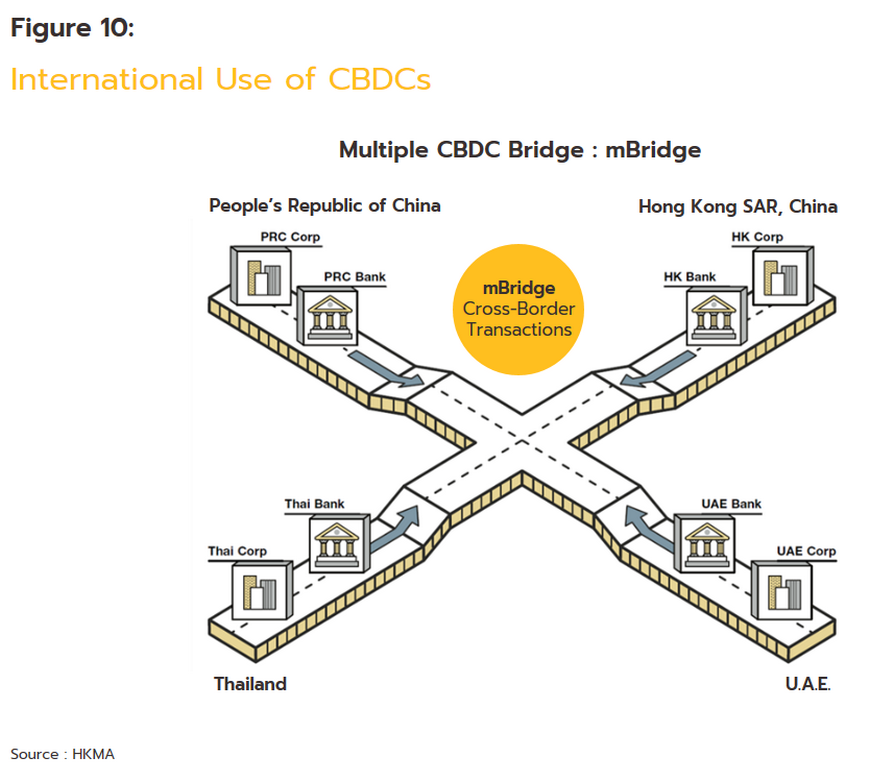

1) ประเภทธุรกรรมที่รองรับ: CBDC สามารถแบ่งออกเป็น CBDC แบบค้าส่งและค้าปลีก แบบแรกใช้เพื่ออำนวยความสะดวกในการทำธุรกรรมระหว่างธนาคารกลางและธนาคารพาณิชย์หรือสถาบันการเงินอื่น ๆ ในขณะที่ลูกค้ารายย่อยของธนาคารใช้แบบหลัง

การจัดประเภท CBDCs โดยคำนึงถึงขอบเขตการใช้งานหรือประเภทของธุรกรรมที่สนับสนุนเป็นรูปแบบการจัดหมวดหมู่ที่พบได้บ่อยที่สุด การใช้ CBDC ในการทำธุรกรรมระหว่างธนาคารพาณิชย์หรือส่วนอื่น ๆ ของภาคการเงินนั้นจัดอยู่ในขอบเขตของ CBDC ขายส่ง และในกรณีนี้ การใช้งานจะช่วยเพิ่มประสิทธิภาพในการทำธุรกรรมให้เสร็จสมบูรณ์และมีการชำระบัญชีความปลอดภัย เช่นเดียวกับ ลดความเสี่ยงด้านเครดิตของคู่สัญญา ในปัจจุบัน มีความสนใจอย่างมากในการใช้ CBDC สำหรับขายส่ง การวิจัยเกี่ยวกับการใช้งานของพวกเขากำลังดำเนินการในวงกว้าง และในบางกรณี พวกเขากำลังเริ่มนำไปใช้ในภาคสนาม การใช้งานของพวกเขากำลังดึงดูดความสนใจเป็นพิเศษในด้านการชำระเงินข้ามพรมแดน ซึ่งความร่วมมือระหว่างธนาคารกลางกำลังถูกผลักดันไปข้างหน้าโดยกลุ่มเล็กๆ เหล่านี้ นอกจากนี้ CBDC แบบขายส่งสามารถใช้ในประเทศในการทำธุรกรรมระหว่างสถาบันการเงินได้อย่างชัดเจน โดยธนาคารกลางจะทำหน้าที่เป็นตัวกลางระหว่างสิ่งเหล่านี้ แม้ว่าเพื่อเพิ่มประสิทธิภาพและความสะดวก ผู้เล่นในภาคการเงินที่สามารถใช้ CBDC แบบขายส่งด้วยวิธีนี้โดยทั่วไป บันทึกธุรกรรมเหล่านี้ในบัญชีแยกประเภทแบบกระจายหรือบล็อกเชน ดังนั้น ดร.อรุณา ชาร์มา อดีตเลขาธิการและสมาชิกของคณะกรรมการธนาคารกลางอินเดียว่าด้วยการเพิ่มพูนการชำระเงินแบบดิจิทัลจึงกล่าวว่า CBDC แบบขายส่งสามารถถูกมองว่าเป็น ธนบัตรที่ไม่ใช้แล้วไปยังธนาคารพาณิชย์ ซึ่งสามารถกระจายไปสู่ระบบเศรษฐกิจในวงกว้างต่อไปได้” [6]

ในทางตรงกันข้าม หาก CBDC สามารถเข้าไปอยู่ในมือของผู้บริโภคได้ สิ่งเหล่านี้จะถือว่าเป็น CBDC ค้าปลีก ซึ่งจะกล่าวถึงในรายละเอียดในบทต่อไป

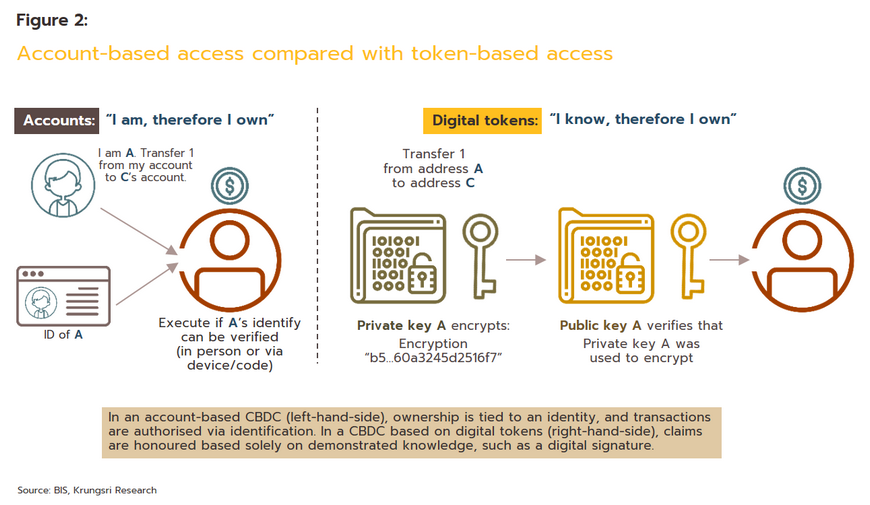

2) CBDC ที่ใช้โทเค็นหรือตามบัญชี

CBDC ตามบัญชีถูกสร้างขึ้นจากพื้นฐานของบัญชีแต่ละบัญชี สิ่งเหล่านี้ใช้เพื่อจัดเก็บข้อมูลที่เกี่ยวข้องกับการทำธุรกรรมทั้งหมดที่เชื่อมต่อกับบัญชีนั้นพร้อมกับยอดเงินคงเหลือ ธุรกรรมเหล่านี้เชื่อมโยงกับข้อมูลที่ระบุตัวตนซึ่งระบุผู้ที่ทำธุรกรรมในลักษณะเดียวกับอีเมลที่เชื่อมโยงกับที่อยู่อีเมลของผู้ส่งและผู้รับ ดังนั้นจึงไม่มีการเปิดเผยตัวตนในระบบนี้เพียงเล็กน้อย ในทางตรงกันข้าม CBDC ที่ใช้โทเค็นนั้นมีพื้นฐานมาจากโทเค็นและเป็นสิ่งเหล่านี้ที่บันทึกข้อมูลที่เกี่ยวข้องกับธุรกรรมซึ่งอาจเชื่อมโยงกับข้อมูลที่ระบุตัวบุคคลหรือไม่ก็ได้ ในระบบเหล่านี้ การยืนยันตัวตนจะดำเนินการผ่านการใช้ลายเซ็นดิจิทัล ดังนั้นระบบที่ใช้โทเค็นจึงมีศักยภาพในการไม่เปิดเผยตัวตนมากกว่าทางเลือกที่ใช้บัญชี อย่างไรก็ตาม เส้นทางดิจิทัลที่พวกเขาทิ้งไว้หมายความว่าระบบที่ใช้โทเค็นยังคงไม่เปิดเผยตัวตนน้อยกว่าเงินสด แม้ว่าระบบดังกล่าวจะมีศักยภาพในการลดความขัดแย้งที่เกี่ยวข้องกับการชำระเงินข้ามพรมแดนได้อย่างมาก

3) CBDC ที่มีดอกเบี้ยและไม่มีดอกเบี้ย

ซึ่งแตกต่างจากเงินสด การใช้ CBDC ช่วยให้ธนาคารกลางมีกลไกในการจ่ายดอกเบี้ยให้กับผู้ถือ CBDC อย่างไรก็ตาม การจ่ายดอกเบี้ยเหล่านี้จะมีผลกระทบต่อกลไกการส่งผ่านนโยบายการเงินของธนาคารกลาง เช่นเดียวกับวิธีที่ธนาคารพาณิชย์จะกำหนดอัตราดอกเบี้ยที่จ่ายให้กับเงินฝากออมทรัพย์และขนาดของเงินฝากโดยรวมที่พวกเขาถืออยู่ (Garratt and Zhu, 2021)

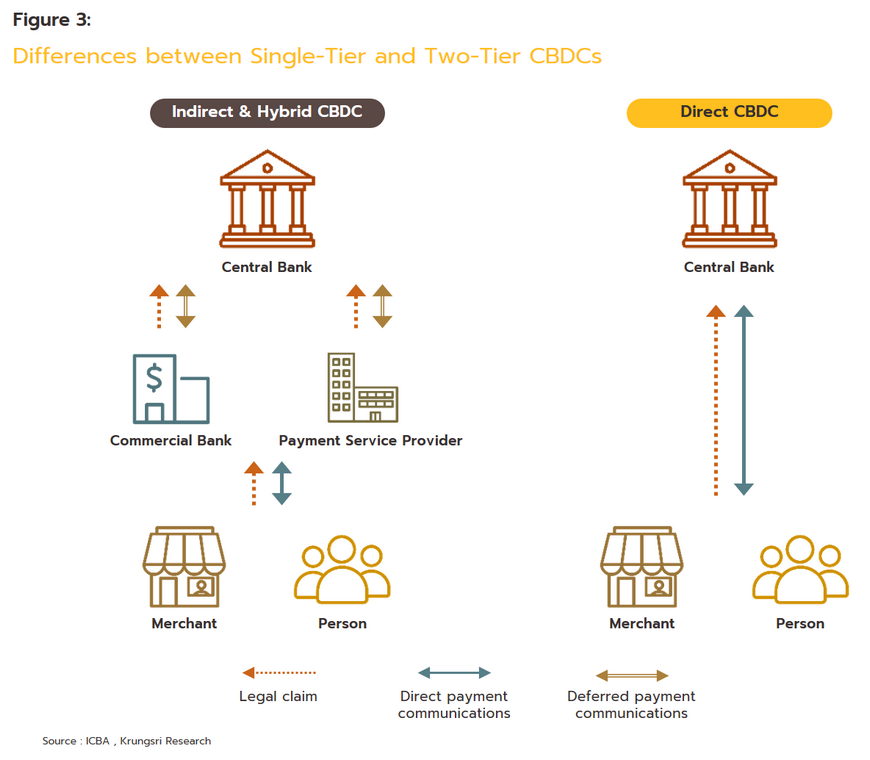

4) ขอบเขตของการมีส่วนร่วมของภาคเอกชน: CBDC อาจแบ่งออกเป็นระดับเดียวและสองระดับตามระดับของการมีส่วนร่วมของภาคเอกชน

ในรูปแบบชั้นเดียว ธนาคารกลางออกแบบสกุลเงินในลักษณะที่พวกเขารับผิดชอบในการดำเนินงานและจัดการทุกจุดของห่วงโซ่การเงิน รวมถึงการติดต่อโดยตรงกับลูกค้ารายย่อย ระบบเหล่านี้จึงเรียกอีกอย่างว่า CBDC โดยตรง อย่างไรก็ตาม หากธนาคารกลางต้องรับบทบาทเหล่านี้ จะทำให้เกิดปัญหาใหม่ที่อาจเกิดขึ้นได้ เนื่องจากในอดีต ธนาคารกลางมักไม่มีปฏิสัมพันธ์โดยตรงกับผู้บริโภครายบุคคล ดังนั้นพวกเขาจึงขาดความรู้และความเชี่ยวชาญในหลาย ๆ ด้านที่สำคัญ เช่น การนำไปใช้ ‘รู้จักลูกค้าของคุณ’ กฎระเบียบ

รูปแบบสองชั้นแตกต่างจากนี้ตรงที่ธนาคารกลางจัดการ CBDC ทางอ้อม และเรียกอีกอย่างว่า CBDC ทางอ้อมหรือไฮบริด ภายใต้รูปแบบเหล่านี้ ธนาคารกลางจะโอนความรับผิดชอบบางส่วนที่คงอยู่ในรูปแบบชั้นเดียวไปยังธนาคารพาณิชย์หรือผู้ให้บริการอินเทอร์เฟซการชำระเงินอื่นๆ เนื่องจากสิ่งเหล่านี้มีความเชี่ยวชาญในการจัดการกับลูกค้ารายย่อย ในเวลาเดียวกัน ธนาคารกลางจะสงวนอำนาจในการออกและอนุญาตการโอน CBDC ไว้สำหรับตัวเอง ด้วยข้อได้เปรียบโดยธรรมชาติของระบบนี้ จึงเป็นตัวเลือกที่ได้รับความนิยมมากกว่าจากทั้งสองตัวเลือกนี้

5) รากฐานทางเทคโนโลยีของ CBDC: เทคโนโลยีที่ใช้ในการบันทึกธุรกรรมอาจขึ้นอยู่กับเทคโนโลยีบัญชีแยกประเภทแบบรวมศูนย์หรือแบบกระจายอำนาจ

เมื่อ CBDC สร้างขึ้นบนระบบรวมศูนย์ ผู้ที่ต้องการชำระเงินจำเป็นต้องเชื่อมต่อกับผู้ให้บริการข้อมูลกลาง ซึ่งอาจเป็นธนาคารกลางหรือธนาคารพาณิชย์ จากนั้นจะรับผิดชอบในการอนุมัติการชำระเงินและปรับยอดคงเหลือในบัญชีให้สอดคล้องกัน ในทางตรงกันข้าม ในระบบกระจายศูนย์ เมื่อมีการทำธุรกรรม ข้อมูลจากบัญชีที่เกี่ยวข้องจะถูกทำซ้ำและกระจายไปยังโหนดเครือข่ายทั้งหมดที่ดำเนินการโดยผู้ตรวจสอบที่ได้รับอนุญาต ซึ่งจะยืนยันหรือปฏิเสธการทำธุรกรรม สิ่งนี้คล้ายกับวิธีการทำงานของ cryptocurrencies เช่น bitcoin แม้ว่าจะมีความแตกต่างที่สำคัญมากตรงที่ bitcoin เป็นระบบเปิดและทุกคนสามารถเข้าร่วมใน blockchain โดยไม่ได้รับอนุญาตล่วงหน้า ในขณะที่ระบบธนาคารและการชำระเงินจำเป็นต้องเปิดให้เฉพาะผู้เข้าร่วมที่ได้รับการยืนยันเท่านั้น ในกรณีของ CBDC สองชั้น การโต้ตอบระหว่างผู้ให้บริการอินเทอร์เฟซการชำระเงินและธนาคารกลางจะถูกบันทึกโดยตรงในบัญชีแยกประเภทของธนาคารกลาง ในขณะที่บันทึกการโต้ตอบระหว่างผู้ให้บริการการชำระเงินและผู้ใช้แต่ละรายอาจอิงตามหลักการที่ควบคุมระบบแบบกระจาย (กล่าวคือ พวกเขา จะใช้การเข้ารหัสและความสามารถในการโปรแกรมอย่างกว้างขวาง) คุณลักษณะหลักอีกประการหนึ่งที่ทำให้ระบบเหล่านี้แตกต่างจากสกุลเงินดิจิทัลคือการออกสกุลเงินใหม่และการควบคุมปริมาณเงินโดยรวมจะยังคงอยู่กับธนาคารกลาง

CBDC รายย่อย: ก้าวสำคัญสำหรับธนาคารกลาง

ตามที่อธิบายไว้ข้างต้น CBDC รายย่อยเป็นรูปแบบหนึ่งของสกุลเงินดิจิทัลที่ออกโดยธนาคารกลาง แต่ลูกค้ารายย่อยอาจใช้ หรืออีกนัยหนึ่งคือสมาชิกสาธารณะ ดังนั้นธนาคารกลางในหลายๆ ประเทศจึงเห็นว่าสิ่งเหล่านี้เป็นช่องทางในการช่วยให้ผู้บริโภคเข้าถึงระบบการชำระเงินที่น่าเชื่อถือและมีความปลอดภัยสูงได้อย่างง่ายดาย และช่วยลดความเสี่ยงด้านเครดิตที่เกี่ยวข้องกับสกุลเงินดิจิทัลอื่นๆ ในทางกลับกัน แม้ว่าเงินสดอาจขาดประสิทธิภาพบางส่วนที่ได้รับจากการใช้สกุลเงินดิจิทัล แต่ก็มีความเสี่ยงน้อยกว่าเนื่องจากได้รับการสนับสนุนจากรัฐบาล และสามารถใช้ชำระธุรกรรมได้อย่างถูกกฎหมาย

.

1. เพิ่มประสิทธิภาพสำหรับทั้งผู้บริโภคและภาคการเงิน

- เร่งการชำระธุรกรรม: ทั้งผู้บริโภคและธุรกิจต้องการสรุปธุรกรรมโดยเร็วที่สุด และ CBDC ค้าปลีกเสนอวิธีหนึ่งในการบรรลุเป้าหมายนี้ เนื่องจากพวกเขาดำเนินการแบบดิจิทัล CBDC ค้าปลีกจึงอนุญาตให้ใช้บริการชำระเงินแบบเรียลไทม์สากลที่เชื่อมโยงข้ามโซนเวลาต่างๆ

- ค่าบริการที่ลดลง: เนื่องจาก CBDC สร้างขึ้นจากรากฐานทางดิจิทัล ต้นทุนที่เกิดขึ้นสำหรับการประมวลผลธุรกรรมแต่ละรายการจึงน้อยมาก และในความเป็นจริงแล้วต้นทุนส่วนเพิ่มอาจใกล้เคียงกับศูนย์ ต้นทุนต่ำเหล่านี้อาจมีข้อได้เปรียบเพิ่มเติมในการกระตุ้นให้ผู้ประมวลผลการชำระเงินของภาคเอกชนลดค่าธรรมเนียมลงด้วย

- การอำนวยความสะดวกในการชำระเงินระหว่างประเทศ: การใช้ CBDC ควรทำให้การทำธุรกรรมข้ามพรมแดนง่ายขึ้น และระบบจะได้รับประโยชน์อย่างมากจากการมีความโปร่งใส ตรวจสอบได้ รวดเร็วและต้นทุนต่ำ (หรือเกือบถึงศูนย์)

2. สร้างการสนับสนุนให้เกิดนวัตกรรมและการแข่งขัน

- ทำให้การเปลี่ยนไปสู่เศรษฐกิจดิจิทัลเป็นไปอย่างราบรื่นและส่งเสริมการใช้สินทรัพย์ดิจิทัลมากขึ้น: เนื่องจาก CBDC ออกโดยธนาคารกลาง จึงเป็นไปได้ที่จะแลกเปลี่ยนสิ่งเหล่านี้กับสินทรัพย์ดิจิทัลประเภทอื่นๆ ได้อย่างง่ายดาย เช่น โทเค็นการลงทุนที่ออกโดยภาคเอกชน ยิ่งไปกว่านั้น เนื่องจากสามารถใช้ CBCDs แทนสกุลเงินที่ไม่ใช่ดิจิทัลได้โดยตรง การทำธุรกรรมเช่นนี้จึงสามารถทำได้ทันที

- การแข่งขันที่เพิ่มขึ้นระหว่างผู้ให้บริการทางการเงิน: เช่นเดียวกับผลิตภัณฑ์ดิจิทัลอื่นๆ ค่าใช้จ่ายที่เกี่ยวข้องในการใช้ CBDC เพื่อชำระธุรกรรมนั้นต่ำมาก และสิ่งนี้มีแนวโน้มที่จะกระตุ้นให้เกิดการแข่งขันที่สูงขึ้นระหว่างผู้ให้บริการชำระเงินภาคเอกชน ซึ่งควรนำไปสู่การปรับปรุง คุณภาพของบริการและการตัดราคาของพวกเขา ในความเป็นจริงแล้ว การใช้ CBDCs นั้นไม่จำเป็นจะต้องใช้สื่อกลางโดยธนาคารพาณิชย์เลย และในทางทฤษฎีก็เป็นไปได้ที่จะชำระธุรกรรมโดยตรงกับธนาคารกลาง สิ่งนี้อาจช่วยแก้ปัญหาที่บุคคลซึ่งถูกแยกออกจากระบบการเงินที่กำลังเผชิญอยู่ในขณะนี้

.

- .

- สร้างบทบาทใหม่สำหรับธนาคารกลาง: เดิมทีธนาคารกลางมีปฏิสัมพันธ์โดยตรงกับสถาบันการเงินอื่น ๆ เท่านั้น แต่ด้วยการสร้าง CBDC รายย่อย บทบาทของธนาคารกลางจะขยายจากการจัดการอุปทานของเงินสู่ระบบเศรษฐกิจไปสู่การมีในทันทีและโดยตรง ความสัมพันธ์กับผู้บริโภครายบุคคล สิ่งนี้จะเปิดโอกาสใหม่สำหรับนโยบายการเงินที่ตรงเป้าหมายมากขึ้น

- .

.

- .

- .

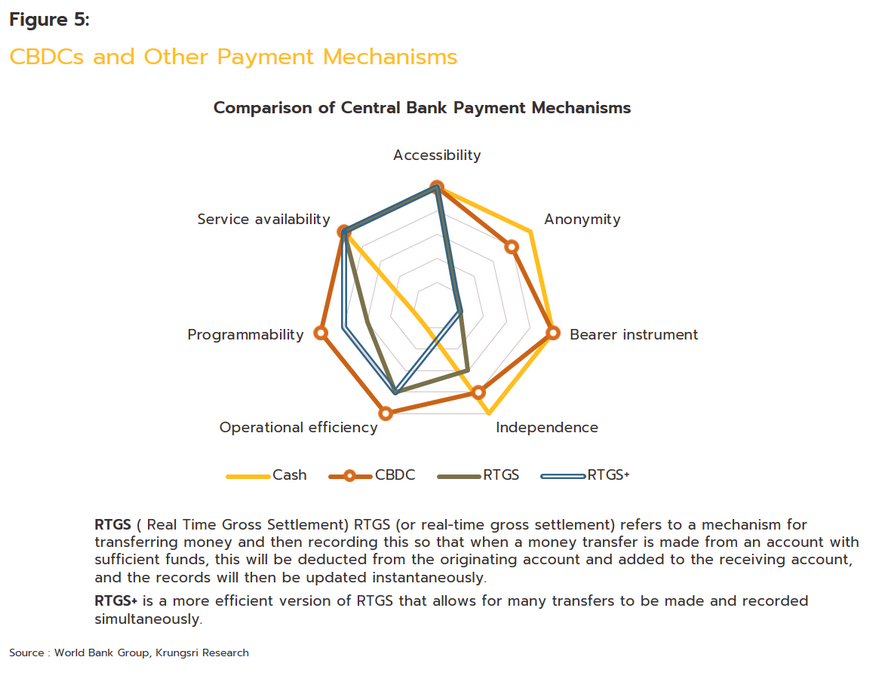

Retail CBDCs and other types of electronic payment systems

- Retail CBDCs and internet and mobile banking

CBDCs overseas

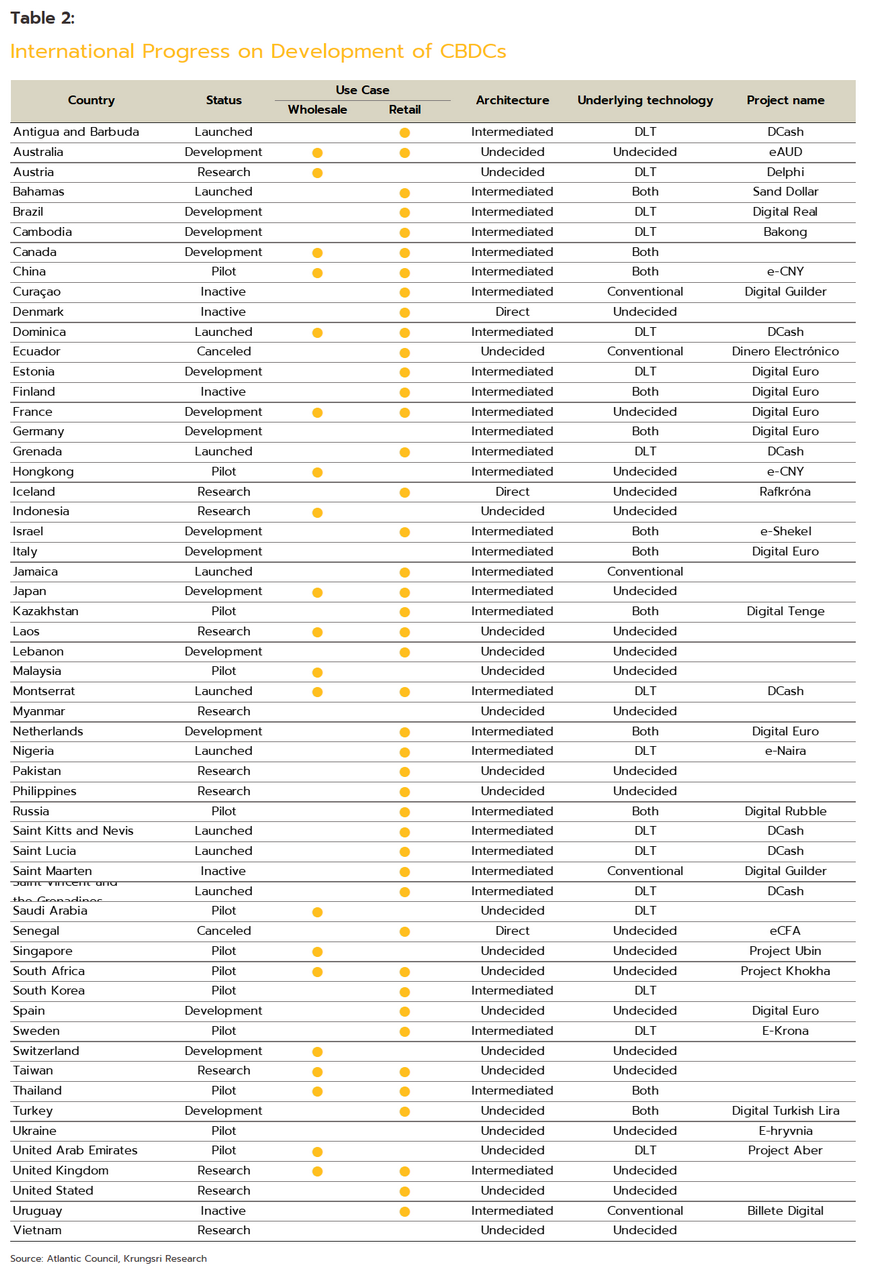

- Research: Countries at this stage of the development cycle are employing academics and other individuals with expertise in financial products to research the implications of developing their own CBDC. This work involves investigating domestic and international case studies and exploring the possible impacts of using a central bank digital currency. 46 countries are currently at this stage, including Austria, Iceland, Indonesia, Lao PDR, Myanmar, Pakistan, Taiwan, the UK, the USA, and Vietnam.

- Development: At this point of the cycle, CBDCs begin to be used in a controlled environment so that their operations can be tested in a way that avoids any risk to the economic system prior to their official deployment in a much wider role. 26 countries are now at the stage of developing their CBDC, and these include Australia, Brazil, Cambodia, Canada, Estonia, France, Germany, Israel, Italy, Japan, Lebanon, the Netherlands, Spain, Switzerland, and Turkey.

- Canceled: A small number of countries have abandoned plans to develop CBDCs having encountered problems that were unforeseen during the research phase. These were then sufficiently troubling to lead to the whole project being suspended and the CBDC being given up, though to date, only Ecuador and Senegal have gone through this.

- Other: Some countries have yet to officially begin work on a CBDC, while others have not revealed how far they have progressed along the path towards developing their own central bank digital currency, even though they may have developed systems to manage digital wallets or built out new domestic payment infrastructure.

Although in general, CBDCs have generated a lot of interest among central banks globally, in Ecuador and Senegal, local difficulties have led to their being abandoned. In the case of Ecuador, the national CBDC, which was called the Dinero Electrónico (DE), was introduced in 2014 but this was withdrawn in March 2018 as problems with its use became overwhelming. The DE suffered from the fact that it could only be used as a payment for transactions that took place domestically (there were problems with using it to pay for international transactions) and the public were confused about the financial structure behind the DE since although it was not backed by the US dollar, it was backed by US dollar-denominated assets. The local media further muddied the waters by incorrectly claiming that the DE was used to support illegal activities and that it infringed users’ privacy, while the private sector never warmed to the project, and in particular, the commercial banking sector remained hostile to the currency’s use, fearing that if the DE gained ground, this would rob banks of their central place in the payment system. In Senegal, the local CBDC, the eCFA, came into use in 2016 but commercial banks were worried about potential confusion between the eCFA and the local currency, the West African CFA franc[13], and this developed into outright opposition that ended with the abandonment of Senegal’s CBDC. With this, the dream that the DE and the eCFA would be the world’s first and longest lived CBDCs came to an end.

The lesson to be drawn from the experiences of Ecuador and Senegal is that in addition to ensuring the currency’s security and the viability of the technology behind it, when developing a retail CBDC, central banks should only gradually roll out the currency to end users and that testing should be thorough and continuous through all stages of development. The new CBDC should therefore be positioned as a payment choice alongside the coins and notes that consumers are already familiar with; this gradual introduction of the CBDC will help the public and business sector become steadily more familiar with the currency, and as this happens, fears and opposition will subside. At the same time, the central bank will need to launch a comprehensive public education campaign to ensure that all parties understand how the CBDC is used domestically, how it is similar to and differs from the normal currency and cryptocurrencies, and how the value of the CBDC is determined and how it may legally be used to make payments. This will then help build confidence in the new currency and assure the public that it is a safe and valid choice for them in both normal and unusual circumstances.

- Users will be able to access their CBDC both when online (for example, through a mobile phone application) and offline (for example, by using a smartcard that facilitates cash-like transactions). This will help to ensure that all members of society are able to use the CBDC and so gain equal access to financial services.

- To ensure equal and fair access, users should not face any kind of charge or fee, payment channels should operate efficiently, and the public should be able to play a role in determining how the CBDC is developed in the future.

- The retail CBDC should be distributed to consumers and to the economy through financial institutions or providers of other financial services since they are skilled in this and have expertise in areas such as confirming personal identities and ‘Know Your Customer’ regulations.

- The CBDC will not pay interest and there will be controls on how much may be exchanged and how much any individual may hold. Prohibiting excessively large withdrawals from the system will help to prevent the economy being destabilized and should protect against the CBDC being used for money laundering.

- The system should draw on the benefits of centralized finance (CeFi), which is able to settle transactions rapidly, and decentralized finance (DeFi), which instead offers stability. As such, consumers will enjoy the highest possible levels of efficiency.

In August 2022[15], the Bank of Thailand released details on its most recent progress with developing a CBDC, and to assess how the CBDC fares in the wild, the bank now plans to begin live testing of a retail CBDC at the end of 2022, though with this initially restricted to a pilot phase. The BOT has also laid out its policies regarding the CBDC and how the design of the retail CBDC may change in the future following work carried out in cooperation with the business sector on establishing the retail CBDC proof of concept. This forthcoming testing phase will be split into two parts.

- During the foundation track, testing will evaluate the efficiency and safety of the system and this will involve using the digital currency in real-life situations. Thus, in this phase of the testing cycle, the retail CBDC will be used to pay for goods and services in a restricted setting, with around 10,000 individuals selected by the BOT participating in the project. Alongside these individuals, 3 private-sector players will be joining the testing, these comprising 2 banks (Krungsri and SCB) and the payment provider 2C2P. These field tests will utilize technology supplied by the German company Giesecke+Devrient[16] and will run from the end of 2022 to the middle of 2023.

- During the innovation track, testing will be extended to investigate how the digital currency’s programmability might be used to extend the CBDC and through this, develop new innovations that use the currency as a platform to meet consumer demand from a broad and varied user base. This will also allow the BOT to refine the development of the retail CBDC and to make it a better fit for the particularities of Thai society. Access to this is open to businesses and members of the public, who were able to present their use cases at the ‘CBDC Hackathon’ that ran from 5 August to 12 September, 2022.

The view from the banking and finance sector

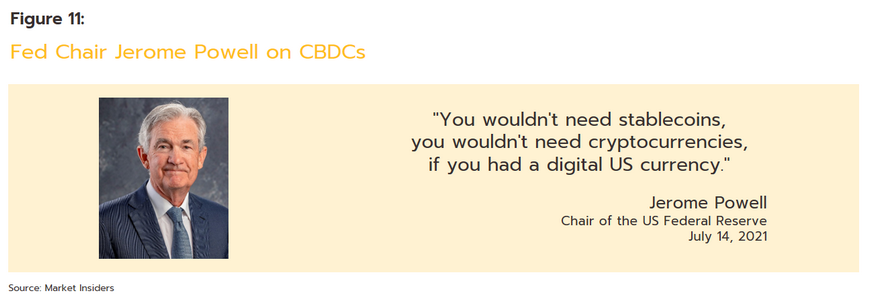

As described above, work on developing CBDCs is underway in central banks around the world, but when these projects reach fruition and CBDCs enter use as a new form of money, the consequences may be significant for stakeholders across the economy, whether that is the state, commercial banks or other financial institutions, the business sector, or consumers themselves. Given the scale of this potential disruption, it is perhaps not surprising that academics and industry experts from within the finance sector have been vocal in expressing their opinions on CBDCs. Among these, Jerome Powell, Chair of the Fed and so perhaps one of the most influential voices in this space, has said that he is broadly pro CBDCs since their introduction would mean that consumers would be less incentivized to hold stablecoins or other types of cryptocurrency. Powell has also said that CBDCs will provide a means by which the public would be able to secure their assets safely, which again marks them out from stablecoins and cryptocurrencies[17].

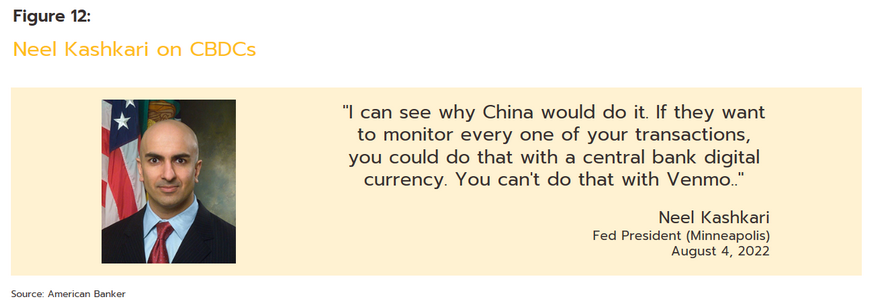

However, although Powell is clearly in favor of them, other influential voices at the Fed are less committed, and Neel Kashkari, president of the Minneapolis Federal Reserve, has expressed worries over potential problems with security and privacy. Kashkari has thus stated that CBDC’s could become a backdoor through which the government is able to spy on the individual transactions carried out by members of the public, and in the case of the USA, using the Venmo[18] system is both convenient and secure from the point of view of individual privacy. Moreover, if individuals would like to speculate on digital assets, Kashkari believes that it is better that they do so through offerings made by private companies that are already active in this space[19].

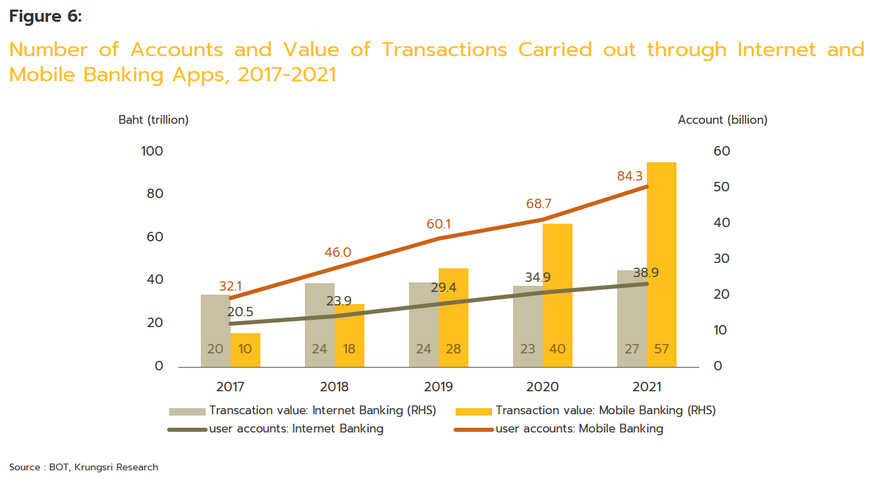

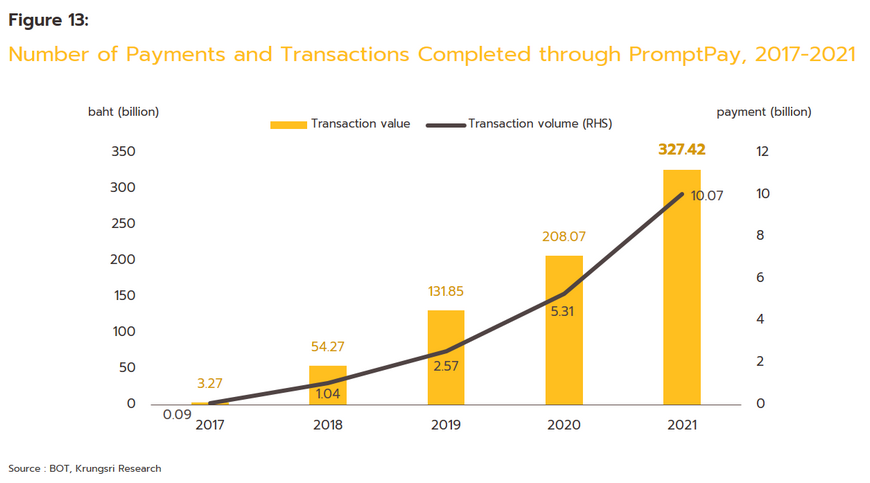

Returning to Thailand and the domestic banking and finance sector, there has recently been a profound change in how this operates, and since 2010 use of internet and mobile banking services to make payments and complete business or shopping transactions has made great strides, with this now a routine and unremarkable feature of daily life. This is especially the case for the PromptPay[20] payment system, use of which received an enormous boost thanks to the outbreak of Covid-19. Throughout the pandemic, officials restricted travel and announced periodic controls on the opening of shops, offices, and places of entertainment, but while these restrictions were in place offline, the online world remained open and free and so consumers were able to carry on their lives there unchanged. Through this, the ubiquity of online payment systems meant that in effect, when consumers were online, they were permanently accompanied by their own virtual bank. As such, demand for in-branch services has crashed and instead the Interbank Transaction Management and Exchange (ITMX) system, which runs behind the scenes to connect domestic banks, has assumed a much greater importance.

However, although internet and mobile banking services have made great inroads into Thai society, a sizeable slice of the population still has a strong preference for cash, and a survey carried out by the Bank of Thailand at the start of 2021[21] showed that at that time, over 65% of respondents planned to return to the use of cash when pandemic-era government stimulus packages ended. By contrast, only 36% planned to increase their use of mobile banking services, and so it is clear that Thai society still has a strong orientation towards the use of cash.

An important question that remains unanswered is therefore whether using a CBDC in place of cash or more familiar internet and mobile banking services has any identifiable benefits for the population at large or exactly where it stands as a value proposition in the eyes of the population. In addition, it is as yet not clear what the consequences of introducing a CBDC will be for the Thai banking system.

Krungsri Research view: CBDCs are a challenge for the commercial banking sector

Over the past 2-3 years, central banks around the world have become increasingly interested in how CBDCs might be developed and deployed. This interest has built against a background of, at least initially, exploding growth in markets for digital assets and a broadening of the user base for these. This process was then sped up further by the 2020-2022 Covid-19 pandemic, which greatly increased consumers’ exposure to how technology could be used to replace many normal day-to-day activities. The global surge in interest in CBDCs is thus further evidence of how digital currencies are moving towards taking a much more central place within the economy.

Nevertheless, one should be careful not to overstate the inevitability of these trends and while it is the case that most countries are pursuing CBDC projects, some are not. Among these, the Danish central bank22/ has yet to identify clear benefits to Danish citizens or to their national payment system of creating a CBDC, largely because the country already has a mature and widely used digital money system. Likewise, as described above, Ecuador and Senegal had previously introduced CBDCs but after only a relatively short period of time, for different reasons both countries were forced to withdraw these.

However, the Thai banking sector is highly developed, is quick to deploy recent technological advances, and because its workforce is skilled and draws on a wide range of disciplines, it has been able to work steadily to improve national payment systems. As such, Thailand’s electronic payments infrastructure is widely recognized as being world-class, and Thai banks compete fiercely against one another to further improve their internet and mobile banking services as they look to better meet consumer needs. Alongside this, the ITMX system provides the back-office services needed to maintain the rapid, seamless and incessant interchange of data between banks, and the outcome of this situation is that Thai consumers are now used to the benefits that come from having permanent access to easy-to-use but comprehensive financial services. However, the introduction of a CBDC may have significant consequences for the liquidity of financial institutions and their ability to act as intermediaries in financial transactions, as has been shown by the Bank of Thailand. Krungsri Research therefore sees CBDCs posing a continuing challenge to the financial system in several different regards.

Firstly, the CBDC might be developed in such a way that it takes a different path to the internet and mobile banking apps that are now so widely used. It is possible that a retail CBDC could be developed in Thailand that was programmable, and this would then allow it to be used in smart contracts. For example, when certain pre-agreed conditions were met, it would be possible to automatically complete a transaction, or alternatively, it would be possible to program a contract in such a way that if something unusual was detected, the transaction would be canceled. This could also ensure compliance with regulatory and legal requirements, and overall, providing these kinds of abilities to the CBDC would add to the economy’s overall efficiency by, for example, making it much easier to make deposits, withdrawals, transfers, and payments, to check for fraud and money laundering, and to automatically collect tax[23]. Having access to this level of functionality would in practice make the CBDC very similar to Ether (ETH), the world’s second most traded cryptocurrency, and in addition to raising its efficiency, being able to program a CBDC would also help to directly address structural problems with the Thai economy and society. However, on the flip side, producing a CBDC such as this would pose a direct challenge to Thai banks. These might then be forced into a position of upgrading and developing their internet and mobile banking services such that the value proposition that these represented was not simply that they allowed users to make regular banking transactions such as transfers and payments, but rather that they provided users with CBDC-type capabilities.

In addition, CBDCs are typically designed to be used on the internet, so clearly access to this is important. The Office of the National Broadcasting and Telecommunications Commission estimates that indeed, around 50 million Thais have access to the internet, though this means that almost another 20 million do not and so for the time being, these individuals are not able to take advantage of commercial banks’ internet and mobile banking services. With internet access very patchy in some communities, the CBDC is likely to be designed in such a way that it can be used offline without having to depend on internet access. This kind of offline CBDC might be based on a smartcard that uses an intermediary device to complete transactions through an offline payment system (OPS). Alternatively, an offline CBDC could use biometrics-based cryptography to confirm a user’s identity before access to the CBDC is granted, and this could all be stored in some kind of personal electronic hardware that again would not need to connect to the internet to function. However, although there are clear benefits to such a system, it would also have disadvantages in that the offline system would likely impose limits on the number of transactions that could take place and on the total volume of money that could pass through the system. Under this type of arrangement, there would also be the possibility of counterfeit CBDCs being created and used, and indeed, central banks in many countries have raised red flags regarding exactly these possibilities[24].

Finally, because CBDCs are being developed by central banks as digital-native currencies, rather than simply working as an alternative to current payment systems, they should also do more to make life easier in the digital space. Krungsri Research therefore expects that in the coming period, CBDCs may take on a much more prominent role in virtual worlds or in the metaverse[25] since in these cases, CBDCs would have a clear advantage thanks to their programmability. Moreover, their use within the metaverse would be a clear improvement on the current situation because at present, completing a transaction in the metaverse requires exchanging normal currency for a digital variant, which is then generally particular to that platform and so cannot be used in other virtual environments. The ability of developers to encode conditions in CBDCs that need to be met before the currency can be spent or a transaction completed would also allow for controls to be placed on spending in the metaverse. For example, it would be possible to add money to a child’s wallet but to restrict its use so that this could only be spent in schools or in other environments within the metaverse that are suitable for children26/. It is clear from this that the development of virtual worlds will open a broad swath of new use cases for CBDCs. Moreover, holding CBDCs for use in the metaverse will have distinct advantages over other forms of digital currency given CBDCs’ stability and the lack of variability in their value, which will add considerably to users’ confidence in these.

In conclusion, the rapid evolution of the digital environment and the increasing extent to which we will all have to keep a foot in both the regular day-to-day world and newly developing virtual worlds will mean that we will no longer be able to avoid the use of digital currencies. Among the latter, CBDCs’ stability and trustworthiness will mark them out as a preferred choice, and so these will help consumers navigate a world that is increasingly marked by volatility, uncertainty, complexity and ambiguity (the so-called VUCA world).

References

A. Arauz, R. Garratt and D.F. Ramos F (Jun 2021) Dinero Electrónico: The rise and fall of Ecuador’s central bank digital currency. Web. Retrieved Oct 4, 2022 from https://www.sciencedirect.com/science/article/pii/S2666143821000107

A.H. Elsayed and M.A. Nasir (2022) Central bank digital currencies: An agenda for future research. Web. Retrieved July 27, 2022 from https://www.sciencedirect.com/science/article/pii/S0275531922001246

Atlanticcouncil (2022) Central Bank Digital Currency Tracker. Web. Retrieved July 6, 2022 from https://www.atlanticcouncil.org/cbdctracker/

Beartai (2022) Diem-Libra คริปโตเคอร์เรนซีของ Facebook ประกาศปิดตัวแล้ว. Web. Retrieved Aug 30, 2022 from https://www.beartai.com/brief/business/928835

Bigdata (2021) CBDC: ระบบการเงินที่กำลังเปลี่ยนโลก และโอกาสของนักวิทยาศาสตร์ข้อมูล, Part 1. Web. Retrieved Aug 5, 2022 from https://bigdata.go.th/movements/introduction-to-cbdc-1/

Blockchain-review (2020) Blockchain-review : CBDC คืออะไร. Web. Retrieved July 22, 2022 from https://blockchain-review.co.th/blockchain-review/cdbc-central-digital-curreny

Clare Harrop, Cyrus Pocha (Dec 2021) Does the metaverse provide a usecase for central bank digital currency? Web. Retrieved Oct 3, 2022 from https://technologyquotient.freshfields.com/post/102hefa/does-the-metaverse-provide-a-usecase-for-central-bank-digital-currency

Digital Currency. Web. Retrieved July 5, 2022 from https://www.outlookindia.com/business/jamaica-launches-jam-dex-becomes-first-nation-to-legalise-digital-currency-news-201592

Erin English (Mar 2021) Finding a secure solution for offline use of central bank digital currencies (CBDCs). Web. Retrieved Sep 29, 2022 from https://usa.visa.com/dam/VCOM/global/sites/visa-economic-empowerment-institute/documents/veei-secure-offline-cbdc.pdf

IBF Singapore (2020) An Introduction to Central Bank Digital Currencies. Web. Retrieved Aug 10, 2022 from https://www.ibf.org.sg/newsroom/Pages/ibfsg_stories_30.aspx

Investopedia (2022) Cryptocurrency news : Fed Releases Discussion Paper on US Central Bank Digital Currency (CBDC). Web. Retrieved July 18, 2022 from https://www.investopedia.com/fed-paper-on-central-bank-digital-currency-cbdc-5216571

Isabelle Lee (Jul 2021) Fed Chair Jerome Powell says cryptocurrencies and stablecoins won’t be needed once the US has a digital currency. Web. Retrieved Sep 16, 2022 from https://markets.businessinsider.com/news/cryptocurrencies/jerome-powell-cryptocurrencies-cbdc-stablecoins-digital-currency-testimony-2021-7

Jiraboon Narktong (2022) โครงการเหรียญ Crypto ของ Facebook ‘Diem’ อาจไปไม่ถึงฝัน สมาคมพิจารณาขายสินทรัพย์คืนเงินนักลงทุน. Web. Retrieved Aug 31, 2022 from https://siamblockchain.com/2022/01/26/zuckerberg-s-stablecoin-ambitions-unravel-with-diem-sale-talks/

John Kiff (Sep 2022) Taking Digital Currencies Offline. Web. Retrieved Sep 30, 2022 from https://www.imf.org/en/Publications/fandd/issues/2022/09/kiff-taking-digital-currencies-offline

Krungsri Plearn Plearn (2021) รู้ก่อนใช้ “Libra” สกุลเงินดิจิทัลใหม่จาก Facebook. Web. Retrieved Aug 29, 2022 from https://www.krungsri.com/th/plearn-plearn/libra-digital-currency

Kyle Campbell (Aug 2022) Kashkari calls CBDC a threat to privacy, defends regional bank independence. Web. Retrieved Sep 20, 2022 from https://www.americanbanker.com/news/kashkari-calls-cbdc-a-threat-to-privacy-defends-regional-bank-independence

Ndtv (2020) Business: These Countries Are Considering A Central Bank Digital Currency. Here Are Their Timelines And Status. Web. Retrieved July 15, 2022 from https://www.ndtv.com/business/here-are-the-timelines-and-status-of-central-bank-digital-currencies-in-some-countries-2820164

Outlookindia (2022) Jamaica Launches “Jam-Dex”, Becomes First Nation To Legalise

Patrick McConnell (Sep 2021) CBDC – How Dangerous is Programmability? Web. Retrieved Sep 26, 2022 from https://sites.duke.edu/thefinregblog/2021/09/21/cbdc-how-dangerous-is-programmability/

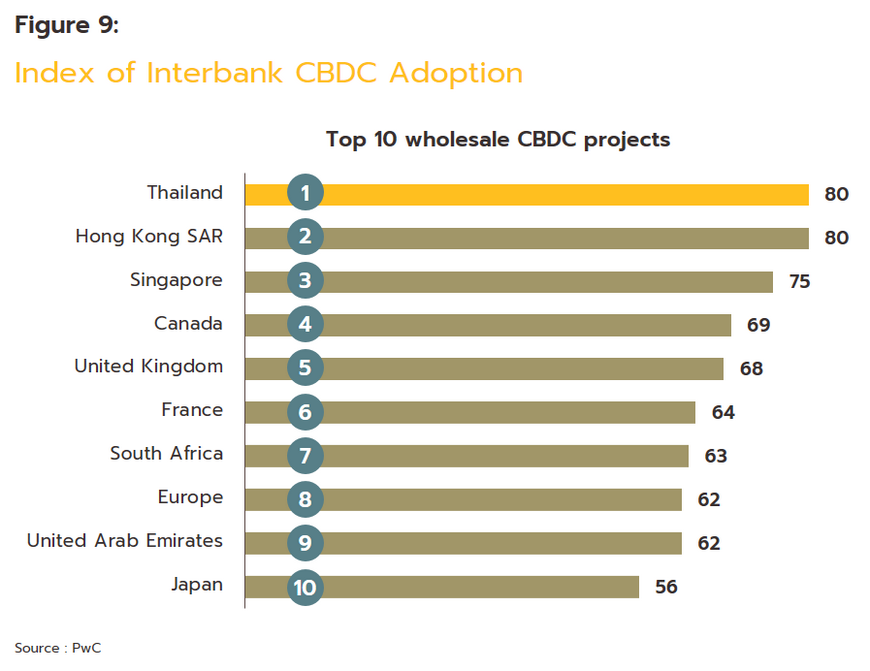

Ploy Ten Kate (2021) PwC เผยไทยติดอันดับ 1 ของโลกด้านการพัฒนาสกุลเงินดิจิทัลแบบ Wholesale CBDC. Web. Retrieved Aug 12, 2022 from https://www.pwc.com/th/en/press-room/press-release/2021/press-release-17-05-21-th.html

R. Morales-Resendiz, J. Ponce, P. Picardo et al. (Mar 2021) Implementing a retail CBDC: Lessons learned and key insights. Web. Retrieved Aug 18, 2022 from https://www.sciencedirect.com/science/article/pii/S2666143821000028#!

Rahul Nambiampurath (2020) How Digital Currency Could Change Senegal’s Financial System Forever. Web. Retrieved Sep 5, 2022 from https://beincrypto.com/how-digital-currency-could-change-senegals-financial-system-forever/

Rodney Garratt, Haoxiang Zhu (Sep 2021) On Interest-Bearing Central Bank Digital Currency with Heterogeneous Banks. Web. Retrieved Aug 15, 2022 from https://www.mit.edu/~zhuh/GarrattZhu_CBDC.pdf

[1] Cryptocurrencies are encrypted digital currencies that record and confirm transactions on blockchains. For more information, please refer to our papers “Traditional Banking and DeFi: What Role will be Left for Banks if the Financial System is Disintermediated?” and “The role of banks in the new world of NFTs” [2] E-money is a type of money that is recorded and stored on electronic devices, such as chips on a card, or on mobile or internet networks. Before spending any money, e-money users transfer money to e-money service providers that is then credited to them(i.e., as a kind of prepayment) and this then allows consumers to pay for goods or services at outlets that accept this form of payment. Using e-money is convenient because it avoids the problems involved in carrying cash, as well as being quick, since shoppers do not have to wait for change. For more information, please https://www.1213.or.th/th/serviceunderbot/payment/Pages/e-money.aspx [1] Stablecoins are a type of digital asset that have a value that is pegged to a non-digital asset, and this then keeps their value stable. For example, the value of 1 Dai is set at 1 USD, and this should not change. For more information, please refer to our research papers, “Traditional Banking and DeFi: What Role will be Left for Banks if the Financial System is Disintermediated?” and “The role of banks in the new world of NFTs” [4] https://fortune.com/2022/01/25/mark-zuckerberg-stablecoin-diem-sale-talks/ [5] https://www.bloomberg.com/news/articles/2022-01-31/meta-backed-diem-association-confirms-asset-sale-to-silvergate [6] https://www.outlookindia.com/business/all-you-need-to-know-about-wholesale-and-retail-central-bank-digital-currency-cbdc–news-192971 [7] https://www.thaigov.go.th/infographic/contents/details/5634 [8] The Deposit Protection Agency (DPA) is a government agency tasked with responsibility for looking after deposits made by Thai and overseas private citizens and companies that are held by commercial Thai banks. The DPA’s remit covers accounts opened in accordance with the Thai Deposit Protection law and is reserved for deposits made in baht into accounts held in Thailand. This covers money deposited in current accounts, savings accounts, fixed deposit accounts, and certificates of deposit (as yet, digital currencies are not covered by the DPA). At present, deposits are insured up to a total of THB 1 million per account holder per financial institution (note that this is not per account). For more information, please see https://www.dpa.or.th/site/index [9] https://tdri.or.th/2022/01/thinkx_430/ [10] https://www.sec.or.th/TH/Template3/Articles/2564/250164.pdf [11] https://www.bot.or.th/Thai/PressandSpeeches/Press/2021/Pages/n9064.aspx [12] These include Angola, Saint Kitts and Nevis, Antigua and Barbuda, Montserrat, Dominica, St. Lucia, Saint Vincent and the Grenadines, and Grenada. [13] West African CFA franc is the currency used in the 8 independent states in West Africa consists of Benin, Burkina Faso, Cote d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal and Togo. [14] https://www.bot.or.th/Thai/PressandSpeeches/Press/News2564/n6064t_annex.pdf [15] https://www.bot.or.th/Thai/PressandSpeeches/Press/2022/Pages/n3965.aspx [16] Giesecke+Devrient is a German company headquartered in Munich. Its business focuses on printing bank notes, and producing asset smart cards and cash management systems. [17] https://markets.businessinsider.com/news/cryptocurrencies/jerome-powell-cryptocurrencies-cbdc-stablecoins-digital-currency-testimony-2021-7 [18] VEMO is US-based Fintech application for money transfers which is broadly used in the US. [19] https://www.americanbanker.com/news/kashkari-calls-cbdc-a-threat-to-privacy-defends-regional-bank-independence [20] The PromptPay system allows for money transfers to a recipient using a proxy ID. This might be an individual’s ID number, a company registration number, or a telephone number that is linked to an account. [21] https://www.bot.or.th/Thai/BOTMagazine/Documents/PhraSiam0165/BOTMAG1-65.pdf [22] https://coingeek.com/denmark-central-bank-downplays-need-for-new-forms-of-digital-money-including-cbdc/ [23] https://sites.duke.edu/thefinregblog/2021/09/21/cbdc-how-dangerous-is-programmability/ [24] https://usa.visa.com/dam/VCOM/global/sites/visa-economic-empowerment-institute/documents/veei-secure-offline-cbdc.pdf [25] The metaverse is an immersive 3-D environment to which users connect via the internet and that seamlessly mixes the real and virtual worlds. Within the metaverse, users experience the world from a first-person point-of-view, seeing objects and people around them exactly as they do in the real world. Thus, once it is more fully developed, it will be possible to live out one’s life within the metaverse, and people will work, rest, consume entertainment, play games, socialize and engage in shared and joint activities within it, just as they would in offline environments. For more information, please see our paper “The Metaverse: When virtuality becomes reality“ [26] https://technologyquotient.freshfields.com/post/102hefa/does-the-metaverse-provide-a-usecase-for-central-bank-digital-currency