The domestic market for medical devices will expand through 2021 at a rate that will closely mirror that of a year earlier, while exports will continue to enjoy strong growth, and although the severity of Thailand’s 3rd wave of Covid-19 infections has temporarily closed the market for medical tourism and severely undercut the number of domestic patients seeking treatment for less severe conditions, demand for single-use consumables (e.g., latex gloves, surgical masks, syringes, catheters and cannulas) remains on an upward track on both the domestic and export markets.

Over 2022 and 2023, demand for medical devices connected to healthcare and hygiene will increase at home and abroad, supported by: (i) rising rates of ill-health due to the increasing prevalence of non-communicable diseases; (ii) a rebound in the number of foreign patients coming to Thailand for treatment (admissions crashed -97% in 2021); (iii) ongoing investment in hospitals by private-sector healthcare providers; (iv) growing interest in health and wellness by consumers worldwide, including those in Thailand; (v) ongoing demand in Thailand’s main export markets for medical devices and equipment, in particular for latex gloves and syringes/hypodermic needles; and (vi) government policy to promote Thailand as an international medical hub. However, Thai players’ weaknesses in developing high-tech applications and products means that in some product categories, the country is dependent on products sourced abroad and then imported and/or those supplied by foreign operations that have set up production facilities in Thailand, and this situation will tend to stoke more intense competition.

Overview

The medical devices sector includes both medical devices and medical equipment[1]. Considered a high-value industry, accounting for 1.2% of GDP[2] in 2020. The sector has continued to grow in tandem with the rising number of patients and and aging population. Because the products are considered life essentials, the sector is also resilient to changes in economic conditions.

Medical devices and medical equipment can be divided into three categories according to use.

1) Single-use devices are used in general medical treatments and normally not high-tech. The items are meant to be disposed after use. Examples include syringes, hypodermic needles, tubes, catheters, cannulas, disposable gloves and some items used in dentistry or ophthalmology.

2) Durable medical devices normally have a life-span of at least one year. Examples include first aid kits, wheelchairs, medical beds, technical equipment used in medicine, surgery and dentistry, electrical diagnostic tools, and x-ray machines.3) Reagents and test kits include equipment used to diagnose illnesses and conditions and chemical kits used to test samples drawn from patients. For example, to test for blood type before dialysis, pregnancy tests, and to detect HIV infection.

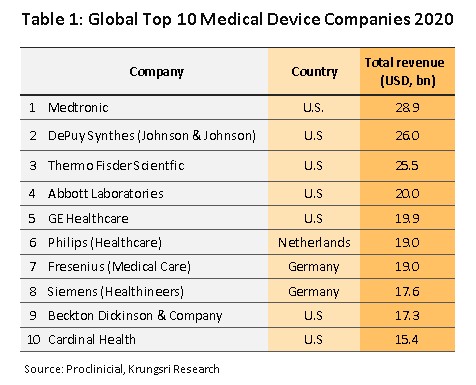

The world’s most important producer of medical devices is the US, and the country therefore enjoys the greatest income from the distribution of medical devices of any nation (Table 1). Although production facilities operated by US corporations are geographically dispersed, output from these is focused on high-value products, such as electro-diagnostic devices, equipment used in orthopedic and fracture-treatment settings, X-ray machines, and dental equipment. Also well regarded for the quality of their cutting-edge products are Dutch and German manufacturers, the latter in particular earning plaudits for their ongoing innovation of production processes. Within Asia, given its role as another world-leading center of innovation, Japan is widely regarded as a leader in the medical devices industry, while players in China and the ASEAN zone tend to be much more heavily focused on the production of consumables. In these countries, high-tech appliances need to be imported, most often from the US, Germany and Japan.

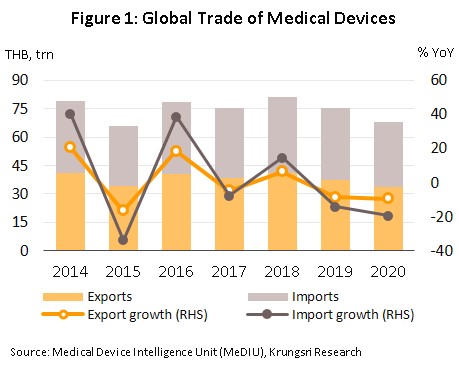

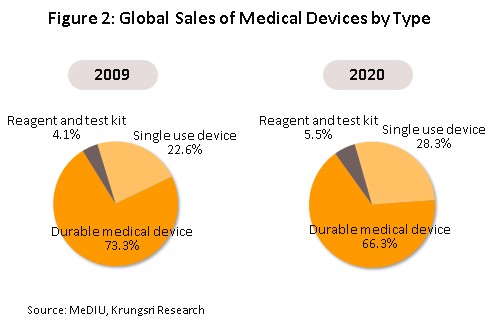

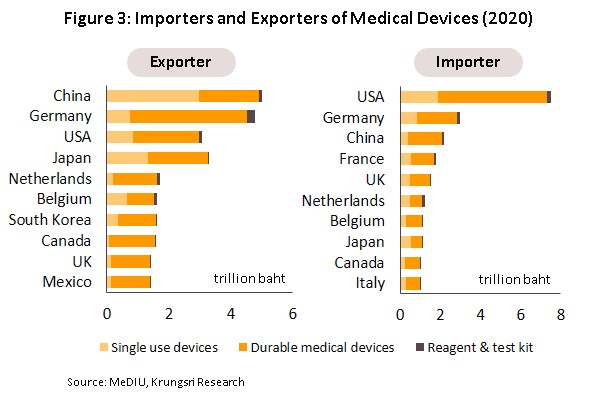

In 2020, the value of medical devices traded on the global market (combined imports and exports) contracted by 9.7% down from in 2019 (Figure 1). The spread of Covid-19 outbreak drives demand for essential medical devices. Products will be prioritized to serve domestic market. The majority of these products were durable items which comprised 66.3% of total global trade (Figure 2), but the value in global market shrank by 20.5%. However, demand for protective equipment continued to rise on higher demand. As a result, single-use device (28.3%) and reagent and test kits (5.5%) rose by 23.8% YoY and 20.5% YoY, respectively. On export side, in global market, large medical device exporter in 2020 (Figure 3) was China (14.7% of global medical device exports), targeting single-use devices; followed by Germany (14.1%), the US (9.8%) and Japan (6.8%). In 2019, the world’s largest exporters were Germany (14.1%), followed by the US and Japan focusing on durable medical devices. The largest importer was the US (22.1% of total global imports of medical devices), followed by Germany (8.8%), China (6.5%), and France (5.2%). Thailand ranked as the world’s 19th exporter of medical devices (1.2%) and 32nd importer of medical devices (0.5%).

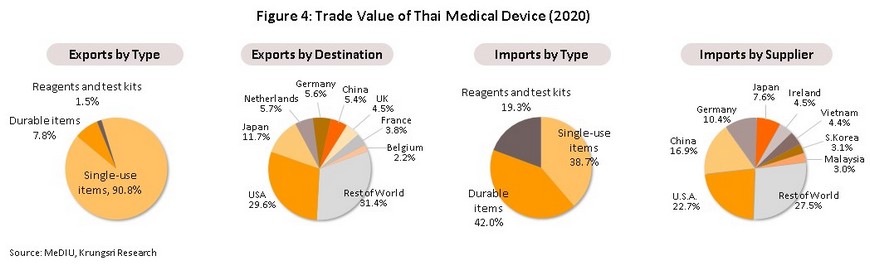

Thailand’s exports of medical devices mostly were single-use devices (e.g. rubber gloves, medical rubber gloves, catheters and medical tubing, syringes and hypodermic needles, and bandages and dressings). which accounted for 90.0% of export value. Thailand’s key export markets are the US, followed by Japan, the Netherlands, and Germany. Most of the manufacturers and exporters in Thailand are foreign-owned companies using Thailand as production base to export to other region, e.g. Japan, the US and France. Looking at imports, these were mostly durable medical items and single-use devices (a combined 80.7% of total import value) e.g. ultrasound equipment, x-ray machines, electrocardiogram (ECG) and electroencephalogram (EEG) monitors, and ophthalmological equipment. The major sources of imports were the United States, China, Germany, and Japan (Figure 4).

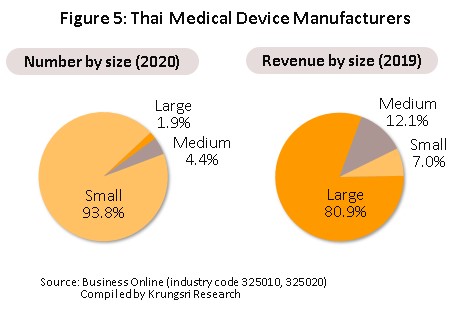

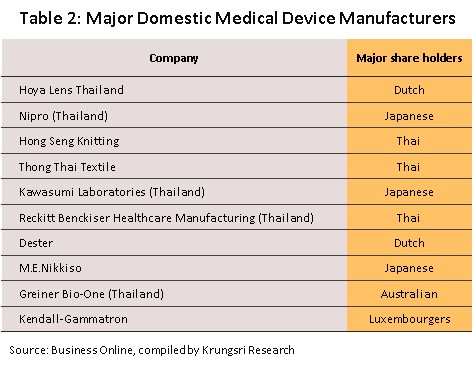

965 producers of medical devices[3] are registered with the Department of Business Development[4] (as of June 2021). Of this, 98.0% are SMEs which recorded a combined 19.1% share of total revenue. Another 2.0% are large manufacturers which command 80.9% of total revenue (2019; Figure 5). Most of those (large manufacturers) are multinational companies (MNCs). They include Nipro (Thailand), Hoya Optics (Thailand), and Kawasumi Laboratories (Thailand) (Table 2). Meanwhile, there are over 2,000 registered importers of medical devices, according to data from the Food & Drug Administration.

Most medical devices produced in Thailand do not require complex technology. The primary output is basic goods that use raw materials such as rubber and plastic that are available in the domestic market. 70% of the total production is aimed at exports. The producers may be classified according to the use of the finished product:

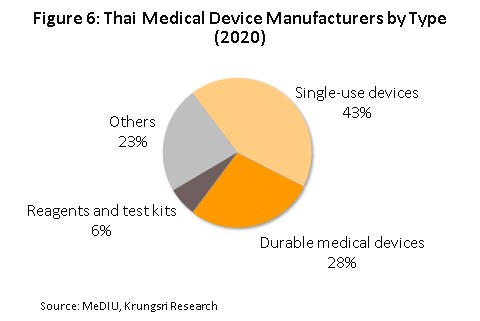

1) Single-use devices: The number of producers in this segment represent about 43% of the total number of medical device producers (Figure 6) up from 39% in 2019. The high-potential and globally–competitive products include rubber gloves/medical gloves because these do not require sophisticated technology. Thailand is also the world’s major producer of rubber (major raw material for production). Therefore, rubber gloves produced are targeted export markets accounting for 90% of total sales of rubber gloves. Other high-potential competitive products are catheters and syringes which are partly made of plastics.

2) Durable medical devices: About 28% of total medical device producers falls into this category. The more important products to manufacture and export are hospital beds, examination tables and wheelchairs, because producers do not require advanced manufacturing technology.

3) Reagents and test kits: Only 6% of manufacturers in the industry produce these, and they are mostly joint ventures with multinationals that want to enter the Thai market. The products include test kits for diabetes, kidney disease, and hepatitis. Between 2015 and 2019, Thailand’s exports of reagents and test kits have surged more than 10-fold[5].

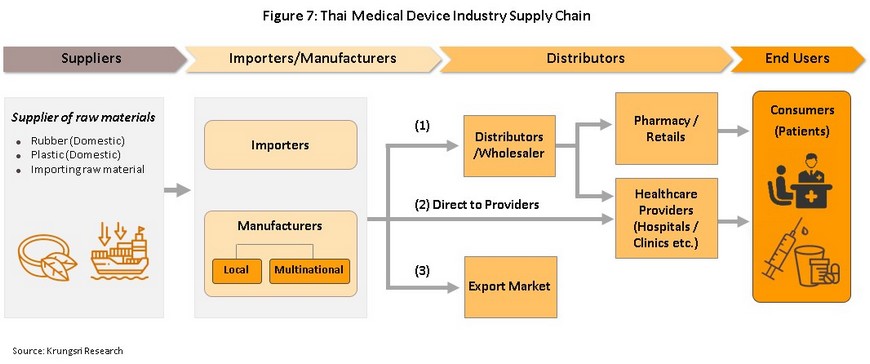

The distribution channels of manufacturers and importers are shown in Figure 7.

1) Distribution to intermediary companies, representatives, or to shops: This includes distribution to companies which are part of the same commercial network as the producer or importer, or to general shops in attempts to reach target customers throughout the country. Players in this group typically have some knowledge of healthcare and are able to exploit a range of distribution channels.

2) Direct distribution to healthcare providers: This includes distribution to public- and private hospitals and clinics. Sales of medical devices to public-sector hospitals is carried out according to government procurement procedures. The Ministry of Finance has changed the purchasing system for public hospitals to the e-bidding process. Under the previous system, purchases up to THB0.1 million can be conducted under an ‘agreed price’, purchases between THB 0.1 million and THB 2 million is subject to the ‘price-checking’ mechanism, and purchase over THB 2 million has to be conducted through competitive bidding. Private hospitals purchasing procedures are not regulated.3) Distribution to export markets: The majority of goods distributed are single-use devices, notably medical rubber gloves. The main markets are the United States, Japan, and Germany. A major player in this group is the Thai Rubber Latex Corporation.

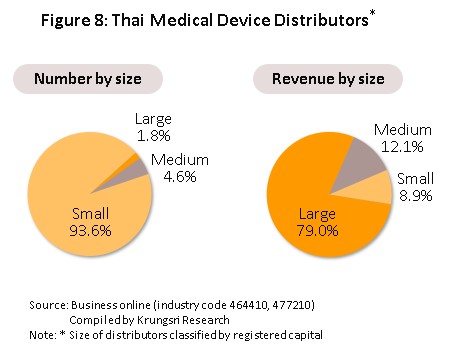

In Thailand, there are over 8,000 wholesale distributors, agents and retailers of medical devices[6]. Most of these are SMEs (98.2%) that command a combined 21.0% of total revenues. Large players which have only 157 (1.8%) but their revenues are much as 79.0% (Figure 8). There is strong competition because of low entry barriers and products are mostly generic, making it easy for consumers to switch to competitor’s products. The major distributors include Zuellig Pharma, Procter & Gamble Trading (Thailand), Pharmahof, B. Braun (Thailand), Biogenetech, Bionet-Asia, and Technomedical.

Limited growth potential for producers and importers of medical devices. (i) Distributors normally focus on selling to hospitals via auction channel, which involves competitive bidding and exposes operators to price competition. (ii) The bulk of imported medical equipment has a long lifecycle, which means replacements are infrequent. (iii) Producers and importers of raw materials, parts, and equipment are exposed to higher costs of imports. This could hurt profitability.

There are several factors to support growth of medical device industry, including expansion of public health services, exports and government’s measures as follows: (i) The Board of Investment is offering tax incentives to manufacturers of medical devices. (ii) The medical devices sector is also one of the new S-curve industries and would benefit from government incentives for investments in the Eastern Economic Corridor (EEC). The government also plans to turn Thailand into a medical hub and expands export of medical devices to the CLMV countries which are seeing rising demand for medical devices (during 2016-2019, Thailand’s exports of medical devices to Lao PDR,, Myanmar, and Vietnam with combined value of 1.5% of total medical devices exports), and, (iii) the 12th National Economic and Social Development Plan (2017-2021) lays out a framework to develop and grow the medical devices sector in line with the 20-Year National Strategy. The framework emphasizes the development of capabilities in areas where there is strong domestic demand and that do not require the mastery of complex technology. This has attracted rising investment in the sector, although this has also led to intense competition as the number of operators increase.

Situation

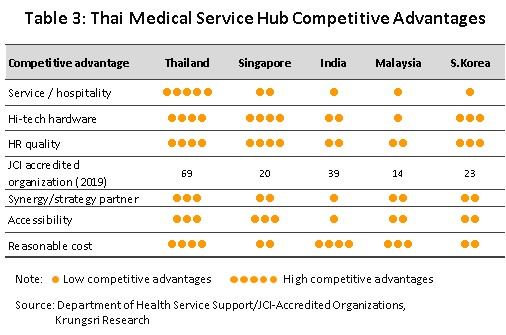

The Thai medical devices industry has seen steady rates of growth in the recent past, and over the period from 2015 to 2019, the value of goods distributed to the domestic and export markets (split approximately 30%-70% by value) rose by respectively 7.8% and 2.7% annually. This growth has been driven by: (i) rising rates of ill health among the Thai population, particularly from non-communicable illnesses (e.g., diabetes and cancer) and the steady aging of Thai society; (ii) the combined effects of government efforts since 2003 to establish Thailand as a medical hub and the high standards and quality of Thai medical care, which have together sustained growth in the domestic medical tourism industry over the past few years (Table 3); and (iii) the establishment of a new policy to make Thailand a center for the export of medical devices to the wider region.

With the exception of single-use devices, domestic demand for medical devices weakened in 2020. As elsewhere in the economy, the Covid-19 pandemic has had considerable impacts, in this context by severely affecting the market for medical tourism and encouraging many domestic patients to postpone or cancel hospital visits for the treatment of non-urgent conditions. However, against this overall weakening of the market, demand for single-use devices (e.g., latex gloves, surgical masks, syringes, catheters and cannulas) jumped on both domestic and export markets. The market was also affected by government moves at the start of the pandemic to control the export of masks (to ensure that domestic supply was sufficient) and its decision to waive import duties on equipment and supplies used to protect against, test for, and treat Covid-19. As such, the year saw considerable disruption to the production, distribution and import of medical devices, as described below.

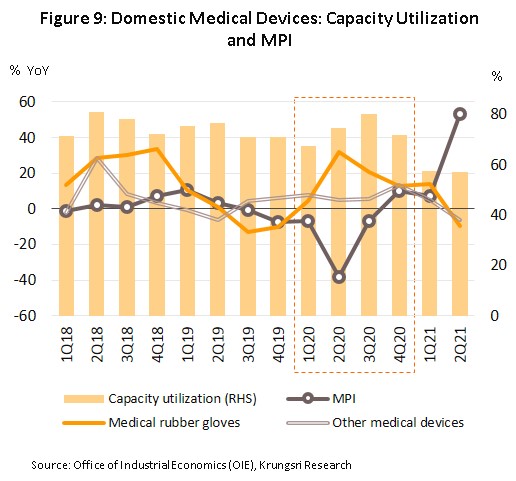

- Overall, output by the industry was in a depressed state through 2020, and for the first time in 4 years, the index of medical device manufacturing output went into reverse and fell -11.0% YoY, partly due to the lockdown that was enforced in April and May 2020 and which then caused production to halt temporarily. The most seriously affected product groups were ophthalmic devices (output was down -13.7% YoY) and equipment for administering blood transfusions and setting up saline drips (-6.9% YoY). On the other hand, output of single-use devices climbed through the year, rising 17.0% YoY for latex gloves, 7.9% YoY for ‘other’ medical devices, and 1.5% YoY for syringes as manufacturers rushed to meet stronger demand on Thai and international markets, though some product groups also benefited from temporary investment support from the government that aimed to encourage production of core items needed during the Covid-19 crisis. The net effect of these divergent trends was then to keep capacity utilization at 73.6%, broadly unchanged from 2019 (Figure 9).

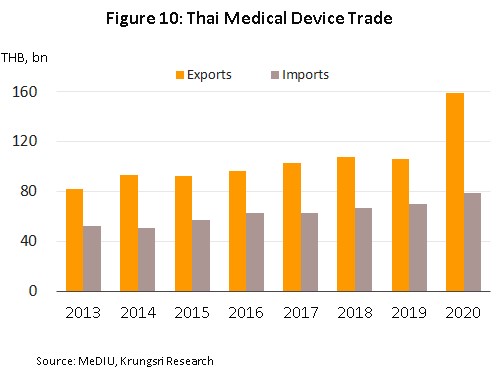

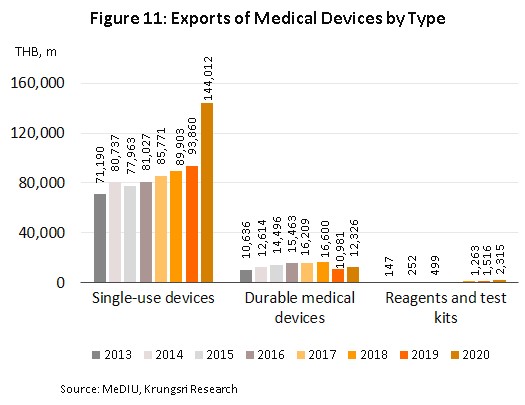

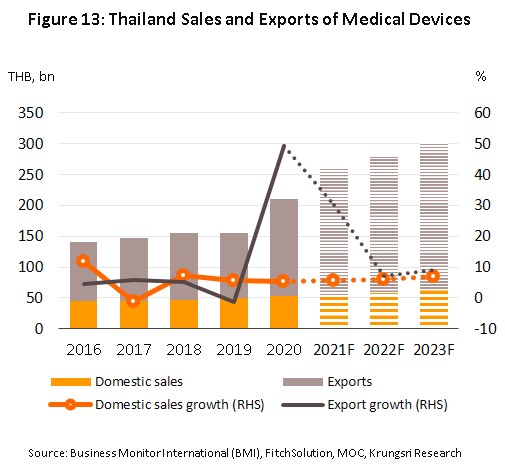

- In 2020, sales of medical devices rose on exports of single-use devices. The value of goods distributed to the domestic market climbed to THB 52 billion, up 5.2% from its 2019 level, and slowed from the annual average of 7.8% maintained over the 5 years between 2015 and 2019 (source: Fitch Solutions). Against this, export value[7] jumped 49.2% to the historic high of THB 15.9 billion (compared to average growth of just 2.7% over 2015-2019) (Figure 10). Sales rose 41.5% to the main export markets of the US, Japan, the Netherlands and Germany (a combined 52.7% share of all exports), 100.3% to China (5.4% of exports), and 36.8% to Lao PDR, Myanmar and Vietnam (a combined 1.3% of exports). Exports of single-use devices (90.8% of all export value of medical devices) rose 53.4% to THB 14.4 billion, compared to average annual increases of 3.1% over 2015-2019, and within this category, the most important product group was latex gloves (51.1% of all exports by value), for which sales surged 117.4%. Gloves were followed in importance by lenses, syringes. Durables items (7.8% of the total), which saw sales increase to THB 12 billion, a rise of 12.2% compared to average growth of 1.0% per year. Finally, reagents & test kits (1.5% of exports) increased 52.7% to THB 2 billion, against average annual growth of 68.8% (Figure 11).

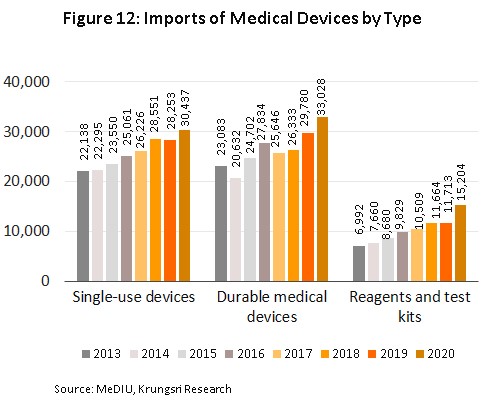

- Import value of medical devices soared by 12.8% to THB78 bn (compared to average growth of just 6.7% over 2015-2019) (Figure 10). The major sources of imports were the US, China Germany and Japan (a combined 57.6% of total import value). By product group, imports of single-use devices (38.7% of import value) increased 7.7% to THB31bn, compared to average growth of just 4.9% over 2015-2019. Durables items (42.0% of value) increased by 10.9% to THB33bn (compared to average growth of just 8.0% over 2015-2019), and reagents & test kits (19.3%) by 29.8% to THB15bn compared to average growth of 9.0% per year (Figure 12). The most imported products were reagents (17.6% of total import value of medical devices) which surged 29.2%, followed by lenses, and medical science devices, respectively.

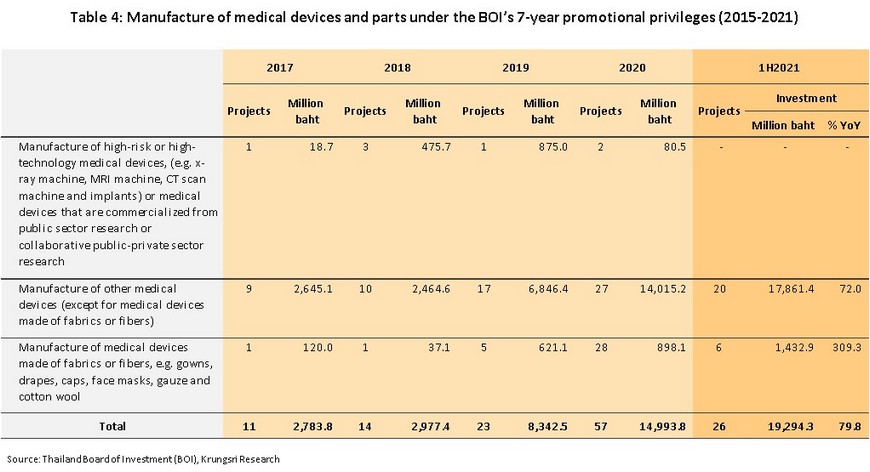

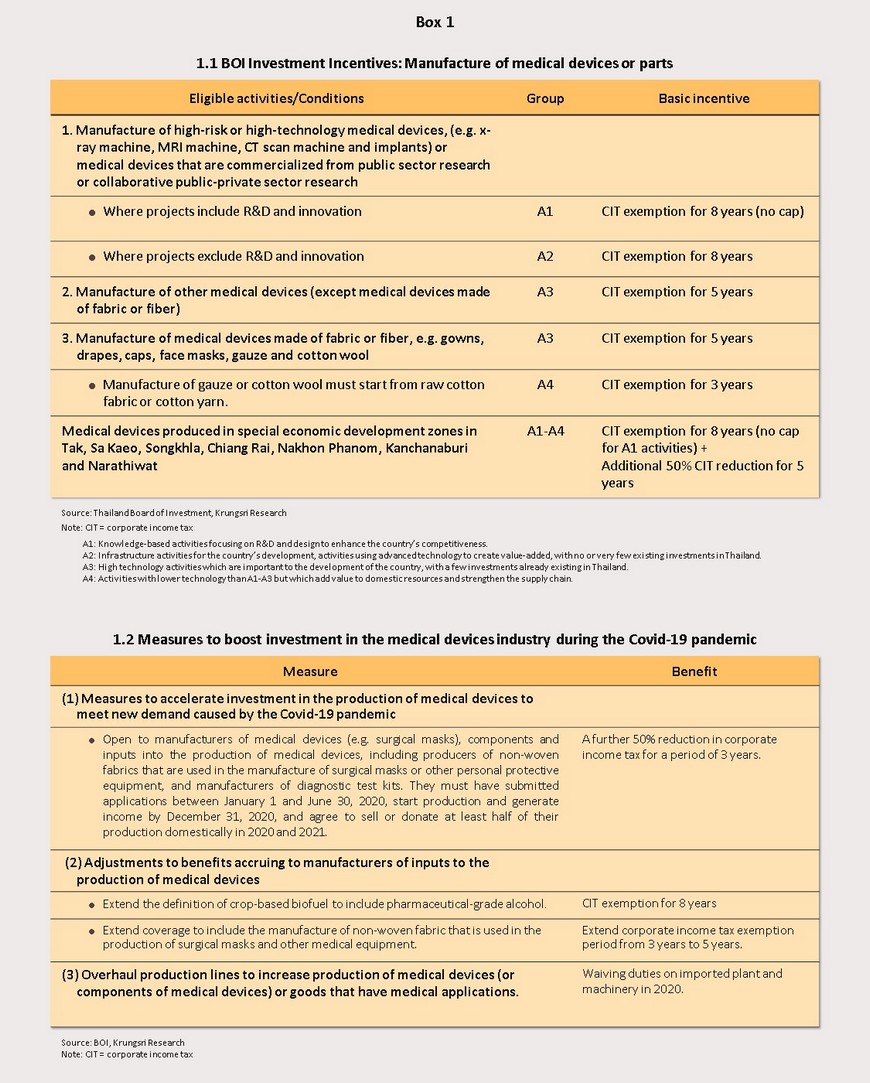

- Investment in the industry also accelerated through 2020. Compared to 2019, the value of projects approved for the government’s 7-year investment support program (2015-2021) jumped 79.7% (Box 1, Table 1.1). Investments made in the ‘other medical devices’ category (excluding goods manufactured from fabric or other woven products or textiles) had the highest total value (THB 14 billion, up 104.7% YoY), followed by fabric-based medical devices (THB 0.9 billion, up 44.6% YoY), but the value of investments in high-risk or high-tech medical devices moved sharply in the opposite direction and crashed -90.8% YoY to THB 80.5 million (Table 4). 6 projects with a value of THB 573.9 million were also approved for investment support under the government’s special program to stimulate the production of goods for which demand was expected to be elevated during the Covid-19 pandemic (Box 1, Table 1.2).

Output by the domestic medical devices industry increased significantly in the first half of 2021 because of the aggravate COVID-19 pandemic situation since early 2021, spurring demand for medical products. Manufacturers speed up production, especially medical devices and personal protective equipment (PPE) and medical equipment for treatment. It is reflected by the Manufacturing Production Index for medical and dental devices increased at accelerated pace by 25.6% YoY, especially production of disposal goods e.g. approved masks, rubber gloves, medical gloves, medical diagnostic test kits. In terms of export markets, exports surged 31.6% YoY to THB96 bn, led by single-uses devices which rose by 37.9% YoY (93.1% of total export value of medical devices, up from 90.8% in 2020). However, exports of durables (5.8% of exports), and reagents & test kits (1.1%) contracted by 19.1% and 16.1%YoY, respectively. At the same time, imports shrank 5.0% YoY to THB 42 bn, led by durables medical devices (36.9% of total imports value of medical devices) which fell by -16.1% YoY. But imports of single-uses (40.4%) and reagents & test kits (22.7% of imports) rose by 1.5 % YoY and 5.6% YoY, respectively. Particularly, imports of reagents (21.3%) surged by 48.0% YoY. For medical industry under the BOI investment promotional privileges, there were 20 approved projects (THB17.9 bn) related to manufacture of other medical devices (except medical devices made of fabrics and or fibers) such as medical rubber gloves, orthodontic appliance, and surgical clamps (surgical clips). The projects rose by 72.0% YoY. Manufacture of medical devices made of fabrics or fibers (e.g. gown, drapes, caps, face mask, and cotton wool) totaled 6 projects worth THB 1.4 bn or up 309.3% YoY (table 4).

The Covid-19 outbreak has pushed Thai manufacturers to rapidly develop easily manufactured products that are perceived to protect against infection by the novel coronavirus (e.g. plastic face shields, cloth face masks and alcohol disinfectant gel). However, more complex and advanced equipment has also been utilized to treat Covid-19 patients, including robots, so that medical staff can maintain a safe physical contact from infected patients. Such robots are being used at Bamrasnaradura Hospital, Rajavithi Hospital and the Central Chest Institute of Thailand. Manufacturers are producing fully-enclosed, fan-equipped laboratory-style personal protective equipment (PPE). As the world awaits the production of a successful vaccine, the pandemic has created an opportunity for players to accelerate the manufacture and export of new products.

Outlook

Krungsri Research sees the domestic and export markets for medical devices expanding in value by respectively 5.7% and 30-35% in 2021. Demand for personal protective equipment (PPE) will continue to strengthen, especially for disposable medical gloves, as will consumption of solutions and diagnostic kits. The government is also working to widen export distribution channels, for example by developing online business matching opportunities for sellers and buyers of medical devices and protective equipment (e.g., PPE suits, syringes, sealed capsules for moving Covid-19 patients in and out of CT scans, and disposable PPE equipment for use in hospitals).

Looking out to 2022 and 2023, Krungsri Research’s analysis indicates that growth in the value of medical devices distributed to the domestic market should average 5.0-7.0% annually. The market will be helped by the completion of the national vaccination program and the suppression of the spread of Covid-19 that this will bring, as well as by economic recovery, even if this is only somewhat sluggish. As the pandemic abates and the economy improves, the number of individuals seeking treatment in hospitals should return to normal levels, and this will naturally underpin stronger demand for medical devices. On export markets, growth is likely to slow from the breakneck pace set over 2020 and 2021 (thanks to the Covid-driven spike in demand for single-use medical devices and especially for latex gloves) to a still impressive 8.0% per year (Figure 13). Individual factors supporting growth in the industry are described below.

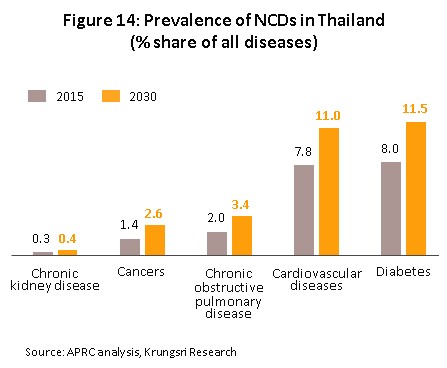

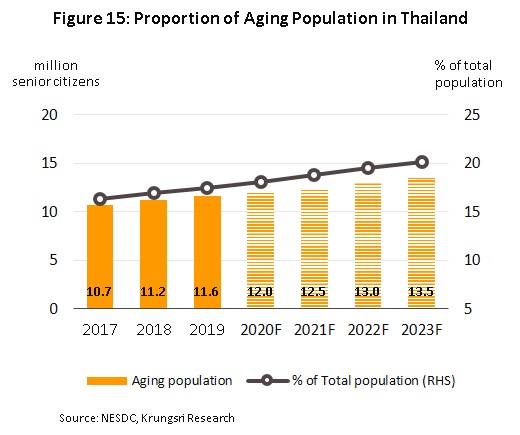

1) health is expected to worsen among the Thai population due to rising rates of non-communicable diseases (NCDs)[8], the most common of which is hypertension, followed by diabetes, chronic obstructive pulmonary disorder, and coronary heart disease (Figure 14). These changes are partly being caused by the aging of Thai society, and the Office of the National Economic and Social Development Council forecasts that the number of individuals over 60 years old in Thailand will increase from 12.5 million in 2021 to 13.5 million in 2023 (Figure 15). In response to this, spending on healthcare for the elderly will come under pressure and this is expected to rise to THB 230 billion (2.8% of GDP) in 2022 from THB 63 billion (2.1% of GDP) in 2010 (Source: 12th National Health Development Plan, 2017-2021). Indeed, currently, the majority of the elderly in Thailand are affected by at least one NCD, most often hypertension (almost half of the over-60s)[9], followed in frequency by diabetes, heart disease, stroke and cancer, and this is then increasing demand for modern, hi-tech medical equipment, especially for use in diagnosis.

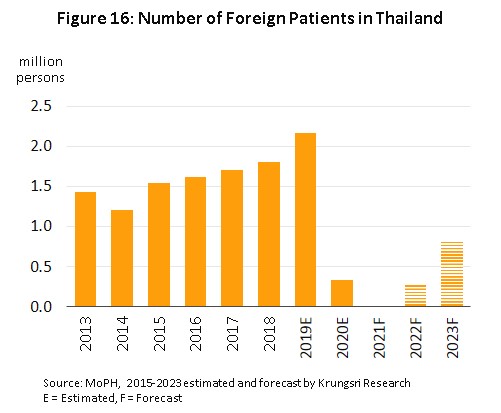

2) Following the -97% slump in admissions in 2021, the number of foreign patients seeking treatment in Thai hospitals is forecast to rebound in 2022 and 2023 (Figure 16). The market will be helped by two main factors. (i) The reopening of major tourist areas is already planned or underway, with Phuket having reopened in July 2021 and other areas due to follow suit once at least 70% of those living in the province are vaccinated. (ii) Thailand occupies a market position as a world-leading player in the medical tourism industry (general and medical tourists account for 80% of foreign patients in Thai hospitals) thanks to: (a) the high quality of the care and services available in its hospitals, and (b) the provision of specialist treatment centers, especially those targeted at conditions such as heart disease, skeletal conditions, cancers, infertility and the care and treatment of the elderly. In addition, Thai facilities are also competitively priced relative to the alternatives (e.g., in Singapore and Malaysia), and these factors will combine to bolster demand for complex medical devices and equipment in the coming period.

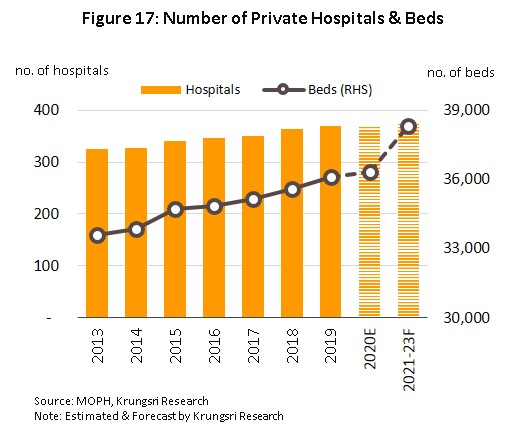

3) To meet increased demand from Thai and overseas patients, many private hospitals plan to increase investments in building new hospitals, expanding existing sites and setting up treatment centers for more complicated conditions. Thus, Bangkok Hospital plans to increase its network from 49 sites to 50 by 2023 and to extend the capacity of existing operations so that it is better positioned to treat specialist conditions. Likewise, Principal Healthcare plans to double the size of its network from 10 sites (as of 2019) to 20 (by 2023), with most of these being located in second-tier cities. Overall, it is therefore expected that over the period 2021-2023, at least 8 new hospitals will be opened and that this will add a minimum of 2,000 beds to total supply (Figure 17), boosting demand for modern, innovative, high quality medical equipment.

4) Interest in personal health and wellness is growing among consumers worldwide, and Thailand has not escaped this trend. One factor behind this is the emergence of Covid-19, which has increased consumer concerns over public health and boosted demand for personal healthcare appliances that can be used at home, for example, portable air purifiers, disinfectant units, sleep monitors, and wearable heart and blood pressure monitors.

5) Exports of medical devices from Thailand should increase in step with the improvement in the general economic outlook in overseas markets. The IMF predicts continuing growth for the US, Japan, Germany, the Netherlands and China (Figure 18), and because combined, these account for almost 60% of all earnings from overseas sales of medical devices, exports of single-use medical devices can be expected to continue strengthening. This is especially so for the US, where sales of latex and surgical-grade gloves remain strong (for 7M21, the proportion of all export income coming from sales of medical gloves to US customers rose from 21.9% to 29.4% of the total). Exports of reagents & test kits to China and Japan also remain solid.

6) The industry has been the beneficiary of government support that has manifested itself in a number of different ways. (i) The government has laid out a plan to establish Thailand as an international medical hub over the years 2017-2026. This plan designates integrated medical services as one of the ‘new S-curve’ industries, thus making investors in the industry eligible for a range of benefits. As part of this, investment promotion schemes are now open to foreign corporations putting money into the manufacture of risky or high-tech devices, such as X-ray and MRI machines, CT scanners, and implantables, or into spin-offs from government-backed research and development, including commercial partnerships with government agencies, but in either case, operators of approved schemes will be eligible for 8-year exemptions from corporation tax. At the same time, manufacturers of medical devices and equipment that set up operations in the special economic zones in Tak, Sa Kaeo, Chiang Rai or Nakhon Phanom or in the Eastern Economic Corridor (EEC) will also be eligible for tax breaks (Box 1). The net effect of these policies should then be to help develop industrial capabilities within the sector, and this will support the research and development of new, lower cost products, as well as strengthening Thailand’s ability to compete on world markets. (In the first half of 2021, 47 applications with a combined value of THB 43 billion were made to the BOI for investment support by players in the medical services industry. This represented a 233.6% rise relative to the same period a year earlier.) (ii) The government has agreed to the implementation of the “Memorandum of Understanding on the Implementation of Non-Tariff Measures on Essential Goods under the Hanoi Plan of Action on Strengthening ASEAN Economic Cooperation and Supply Chain Connectivity in Response to the COVID-19 Pandemic” (November 2020). Under this MOU, ASEAN member states agree not to pass laws or implement regulations that would hinder the free movement of goods that are in high demand due to the Covid-19 crisis, including medicines and medical devices. The agreement will last for 2 years, and so this will help to further boost exports from Thailand to markets in the ASEAN zone.

7) The industry is also benefiting from the development of the innovative, high-tech medical products that are needed as society addresses the challenges posed by the ongoing transmission and evolution of Covid-19. Thus, public- and private organizations are, alongside education and research institutes, developing new medical devices, including positive pressure units, powered air-purifying respirators, contactless self-service check-up machines, low-contact diagnostic and monitoring equipment, and non-woven fabrics that are produced from nanometer to micrometer filaments. The latter are highly protective and are providing a very promising basis for the development of inputs and parts used in new medical devices and equipment, as well as offering a way to cut the country’s dependency on imports (these goods are expected to be ready for commercial distribution some time during the final quarter of 2021). Beyond this, the construction of the new King Mongkut Chaokhun Thahan government hospital has come hand-in-hand with the establishment of Thailand’s first comprehensive research and innovation hospital, and it is hoped that in the coming period, this will lead directly to the development of products that are not just innovative but also commercially viable. In this case, in addition to helping to add value to the medical devices supply chain, these developments will also propel Thailand further towards the goal of becoming a center for the export of medical devices to the world market.

Krungsri Research’s evaluation of opportunities for developing markets for each product group is laid out below.

- Demand for single-use products will grow steadily, driven by the following: (i) rising interest in personal health and hygiene and the effects of government measures to combat the spread of Covid-19, for example by requiring health professionals to wear PPE and wearing face mask in public is required, (ii) expansion of public health services; and (iii) the fact that these are general goods that are used widely in daily life and Thailand benefits from ready-access to upstream inputs, as the world’s leading source of rubber (used in the production of disposable medical gloves), a domestic petrochemical industry (which supplies inputs to produce syringes and catheters), and a textile industry (to produce surgical masks). However, competition is rife in this segment, from both Thai producers and producers in China (surgical masks) and Malaysia (surgical gloves).

- Markets for durables and reagents & test kits are likely to continue to expand. Demand for durables would grow, underpinned by (i) government support for community-level health checks, use of mobile testing centers; and (ii) expansion of existing/construction of new hospitals, which will raise demand for technology-based medical equipment. For reagents and diagnostic kits, those which are used to check for coronary heart disease is expected to see the strongest growth, will be encourage by export market.

Beyond this, developing domestically-produced medical device that will play more important roles in the future will be medical robots and automation[10]. These will be applied for diagnosis, medical treatment, rehabilitation, artificial organ manufacture; for example, the AI is used for diagnostic radiology, robotic sensor system, and remotely-controlled robots that assist with micro-surgery, and automated systems. Development of medical robotics will help reduce dependency on imports of innovations in the long run. In case, the government support for the research & development of commercially viable products in these areas would help to increase the value of exports, reduce dependency on imports, and ensure the sustainable, long-term development of the Thai medical devices industry.

However, alongside the positive factors outlined above, the industry will also need to confront a number of challenges. (i) Competition will tend to stiffen due to Thai manufacturers’ only limited ability to develop high-tech products, which has then made them reliant on goods that are either imported or manufactured by overseas players that have set up production facilities in Thailand (In the first quarter of 2021, 14 submissions were made to the BOI for investment support from projects based in the medical industries. These had a combined value of THB 13.37 billion, or around a quarter of the value of all submissions made to the BOI for overseas investments in the government’s targeted industries). Some examples of these include Japanese operations that use Thailand as a base for the production of facemasks and diagnostic kits, large-scale joint-ventures by Korean and Thai players11/ (e.g., between the Korean Genexine and Thailand’s Kingen Holdings to manufacture precursors for use in the production of biologics), and German involvement in the sector (e.g., the joint venture between HAASE Investment and Siam Bioscience to manufacture biological reagents). (ii) Most players need to source the high-technology manufacturing equipment used on their production lines from other countries and this then exposes them to the risk of exchange rate fluctuations and higher costs for imports. (iii) Production of medical devices will increasingly be concentrated on innovative, high-tech goods, including products used in the care of the elderly, innovative consumables, implants, and parts for electrical and radiation-based diagnostic equipment. (iv) Consumption of single-use medical equipment is likely to rise, but although this provides a high degree of protection against the transmission of disease, its use can also create significant environmental problems because although used equipment may be sterilized, the materials from which it is made are almost never biodegradable. In some countries (e.g., China and India) governments are therefore implementing policies to reduce the environmental impact of waste and supporting research into new materials. The use of biodegradable materials will likely play a major role in helping to cut the negative impacts of medical waste, and developing these products will be a challenge that players in the industry will need to surmount.

Krungsri Research’s view

The severity of the 2021 Covid-19 outbreak in Thailand helped to support greater consumption of medical devices on the domestic market, while at the same time, export growth accelerated on stronger demand, especially for PPE used to protect against Covid-19. Over 2022 and 2023, demand for medical devices related to public health and healthcare will continue to strengthen, and this will then support a solid outlook for the industry as a whole.

- Manufacturers of medical devices: earning are projected to grow satisfactorily and operators will enjoy steady profits, even as competition strengthens. Manufacturers that distribute medical devices and equipment through healthcare facilities will continue to register higher revenues, especially those sell to hospitals that are expanding operations and investing more on medical equipment. Consumers are also taking a greater interest in their health, and this presents an opportunity for players to develop new products and equipment to meet this burgeoning demand. Operators will also be able to develop export markets in neighboring countries by taking advantage of the government’s efforts to promote investment in the EEC, to complement plans to turn Thailand into a medical hub and a regional center for the export of medical supplies and equipment. Nevertheless, despite this generally upbeat assessment, competition is rising within the industry as more international companies invest in production facilities in Thailand to export to customers in the third countries (such as Japan, the United States and France), and operators that need to import parts could face higher costs because they may need to employ currency hedging tools.

- Distributors of medical devices (including retailers, wholesalers and importers): revenue will grow in the next few years, albeit slowly. The majority of goods distributed are disposable items that are used regularly in healthcare facilities and by the unwell, but competition is worsening due to the large number of SME distributors in the market. They are fighting for space with agents and retailers that are part of a manufacturer’s commercial network and have access to wider and more comprehensive distribution channels. This would cap growth in this segment. However, importers of medical equipment are generally large, efficient operations that are skilled in marketing and cost-management. These players are now increasingly importing medical robots for use in private hospitals, for example to assist with micro-surgery and in the production and management of pharmaceuticals. This will support earning growth in the coming period.

[1Medical devices include items which are used in the medical, nursing and midwifery professions to provide treatments for bodily conditions such as X-Ray equipment, ultrasound machines, reagent and test kits, and dental devices. Medical equipment refers to surgical and medical equipment e.g. scalpels, thermometers, blood-pressure monitors, and items such as disposable gloves and masks.

[2]Calculated from domestic sales and export value

[3]Thailand’s medical devices sector operates under the legal provisions of the Medical Devices Act (2008). The Medical Device Control Division under the Food & Drug Administration is the agency responsible for regulating the sector and issuing permits to produce, distribute and import medical devices, subject to specifications and standards laid out by the Thai Industrial tandards Institute. This is aimed at assuring consumers that all medical devices in Thailand meet the same standards, and to build up the competitiveness of the sector and acceptance of Thai products in the domestic and export markets.

[4]Including dental devices and equipment

[5]Detailed Figure 12

[6]This refers to the wholesale and retail of medical products including instruments, tools, equipment, treated bandages, first-aid kits, birth control products, and pharmaceutical products.

[7]Export data collected from Medical Device Intelligence Unit, the Plastics Institute of Thailand

[8]Source: Ministry of Public Health, Fiscal Year 2020 (October 2019 – March 2020)

[9]The Ministry of Public Health states that of 9 million elderly, over 4 million have hypertension and over 2 million have diabetes.

[10]Thailand Center of Excellence for Life Sciences (TCELS) estimates that the global medical robotics market will earn revenue of US$ 46.24 billion in 2022, or average growth of 20% annually from US$ 6.62 billion in 2012.

[11]Investment from 1,000 million baht or more